Solar Market Insight Report 2014 Q3

Share

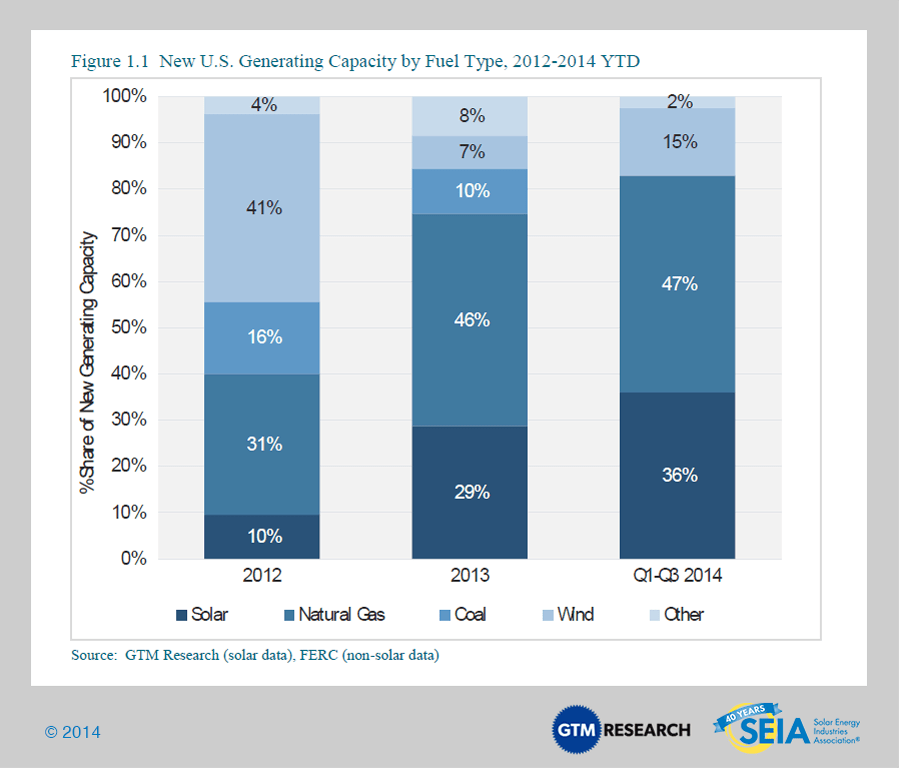

1-1-NewUSGeneratingCapacitybyFuelType.png

(118.67 KB)

{kind=link}

{kind=link}

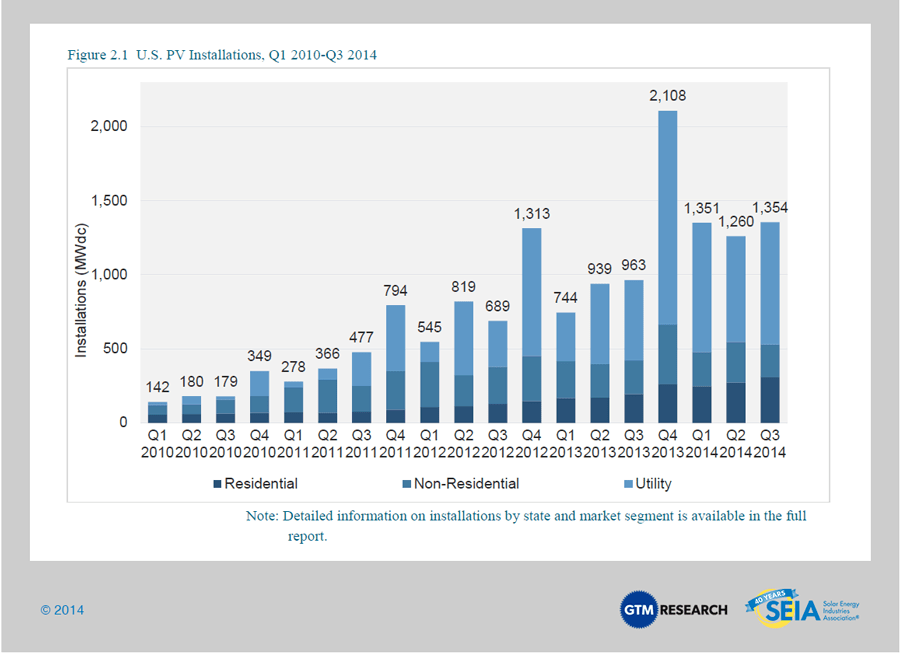

2-1-USPVInstallationsQ1-Q3.png

(116.75 KB)

{kind=link}

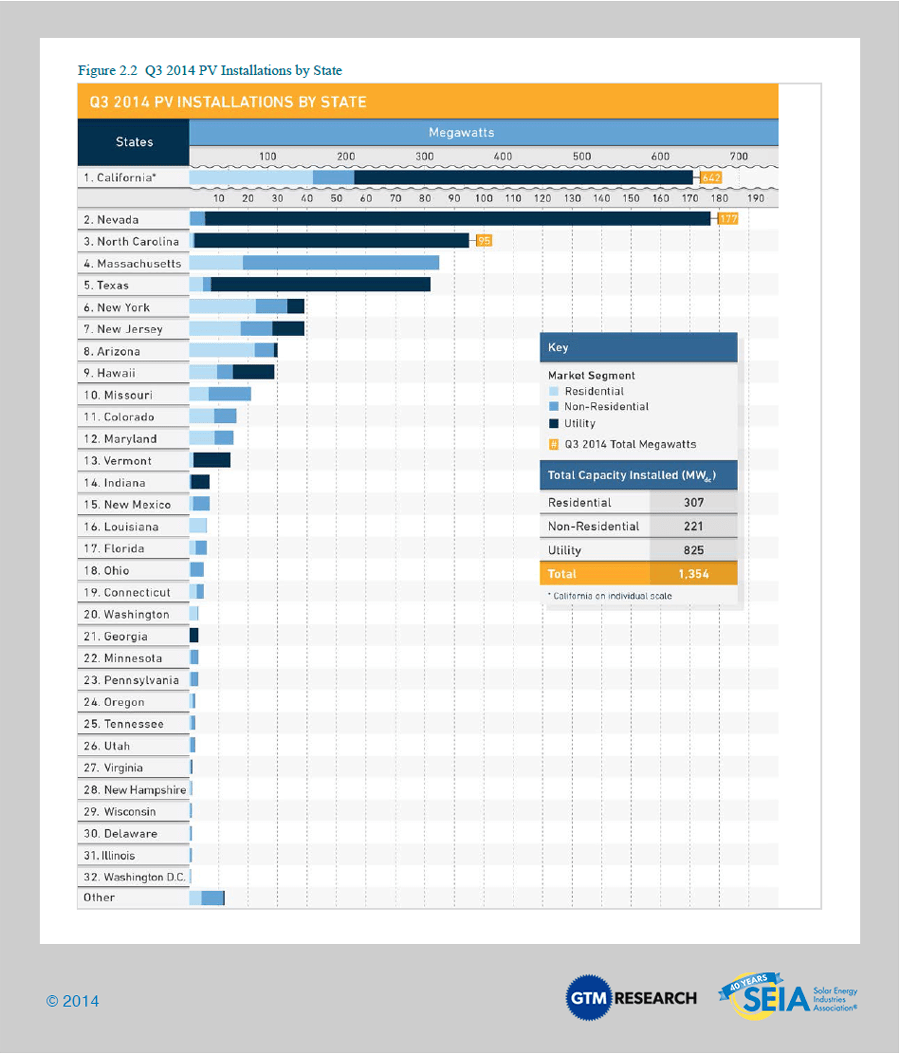

2-2-Q3PVInstallationsByState.png

(373.92 KB)

{kind=link}

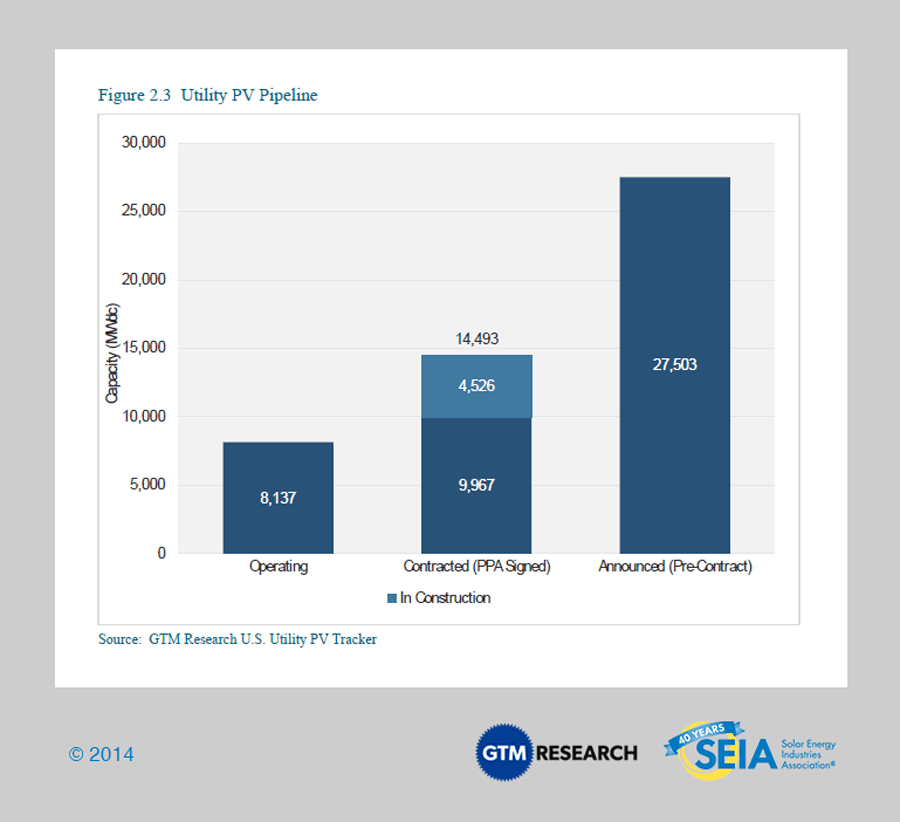

2-3-UtilityPVPipeline.png

(79.39 KB)

{kind=link}

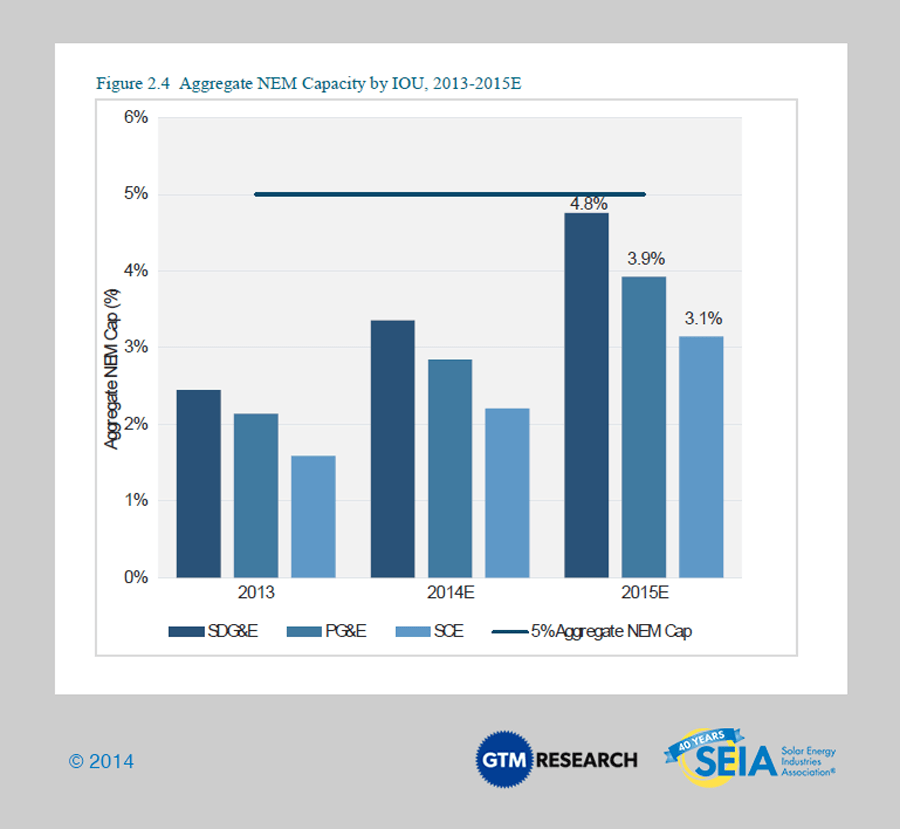

2-4-AggregateNEMCapacity.png

(78.19 KB)

{kind=link}

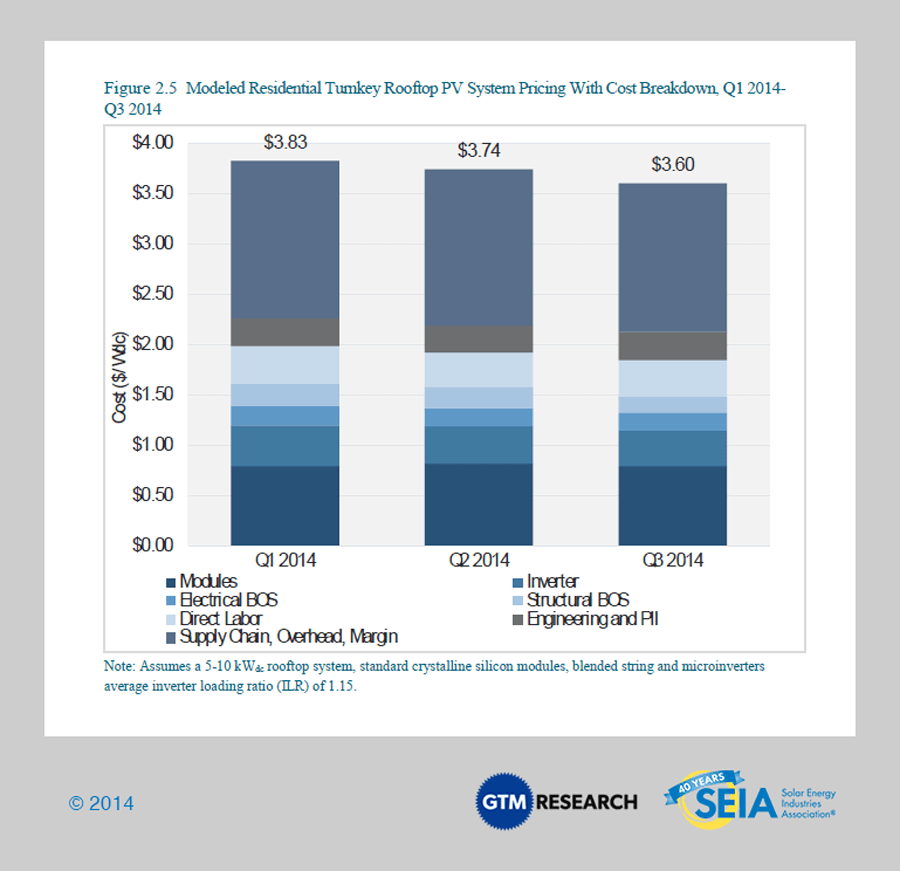

2-5-TurnkeyRooftopPVSystemPricing.png

(129.95 KB)

{kind=link}

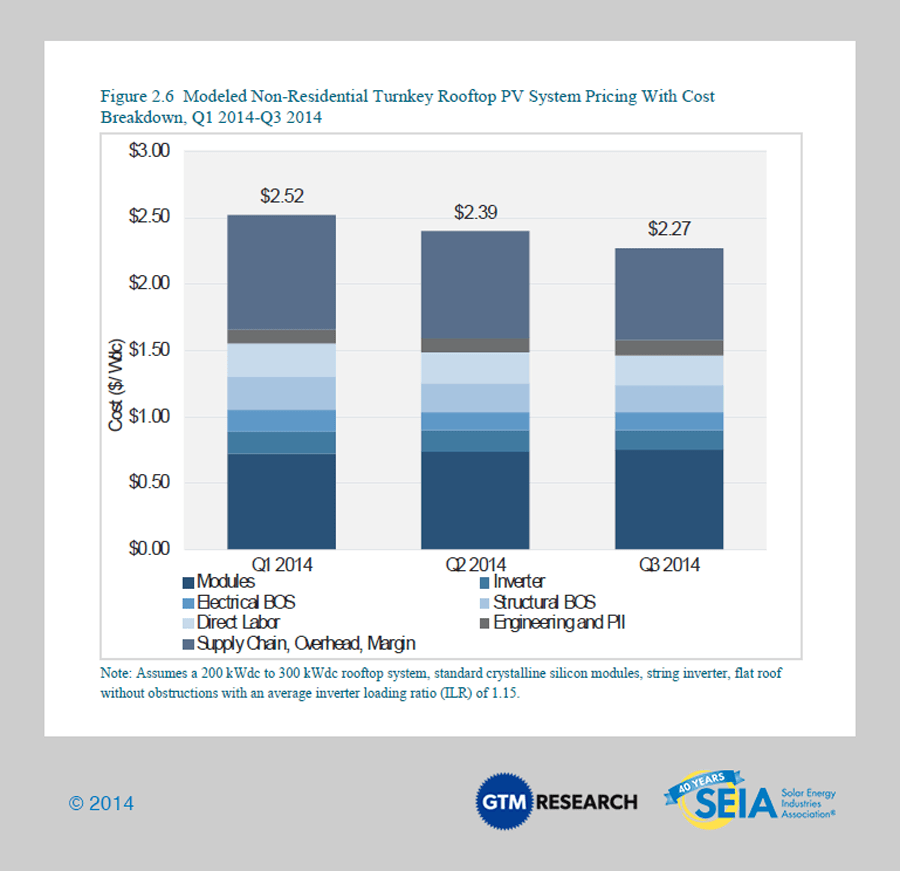

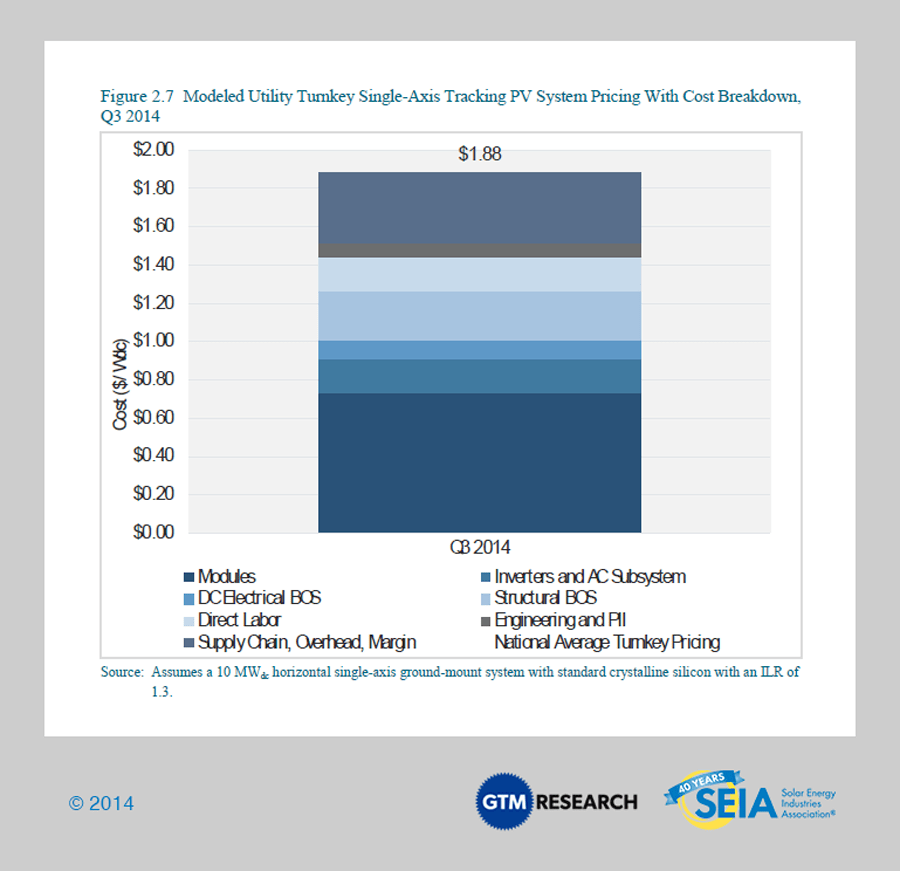

{kind=link}

{kind=link}

2-8-PolysiliconWaferCellModulePrices.png

(119.78 KB)

{kind=link}

2-9-2-10-PVInstallationForecast.png

(93.33 KB)

{kind=link}

2-11-PVInstallationForecastMap.png

(294.43 KB)

{kind=link}

3-1-SelectCSPDevelopmentHighlights.png

(250.51 KB)

{kind=link}

Resource Type

Browse Resources by Related Topics: