Solar Market Insight Report 2015 Q1

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Purchase the Full Report | Press Release

The quarterly SEIA/GTM Research U.S. Solar Market Insight™ report shows the major trends in the U.S. solar industry. Learn more about the U.S. Solar Market Insight Report.

Key Figures

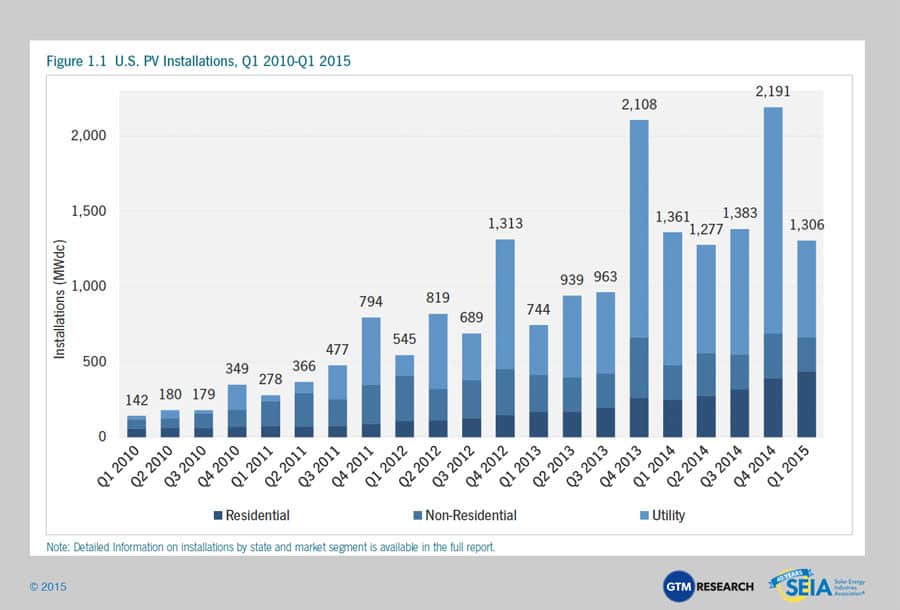

- The U.S. installed 1,306 MWdc of solar PV in Q1 2015, marking the sixth consecutive quarter in which the U.S. added more than 1 GWdc of PV installations.

- Through Q1 2015, nearly one-fourth of cumulative residential solar installations have now come on-line without any state incentive.

- The residential and utility PV market segments each added more capacity than the natural gas industry brought on-line in Q1 2015.

- Collectively, more than 51% of all new electric generating capacity in the U.S. came from solar in Q1 2015.

- Of the 68 MWdc of community solar installations to date, more than one-third of that total has come on-line since 2014.

- More than 5 GWdc of centralized PV has now been procured by utilities based on solar’s economic competitiveness with fossil-fuel alternatives.

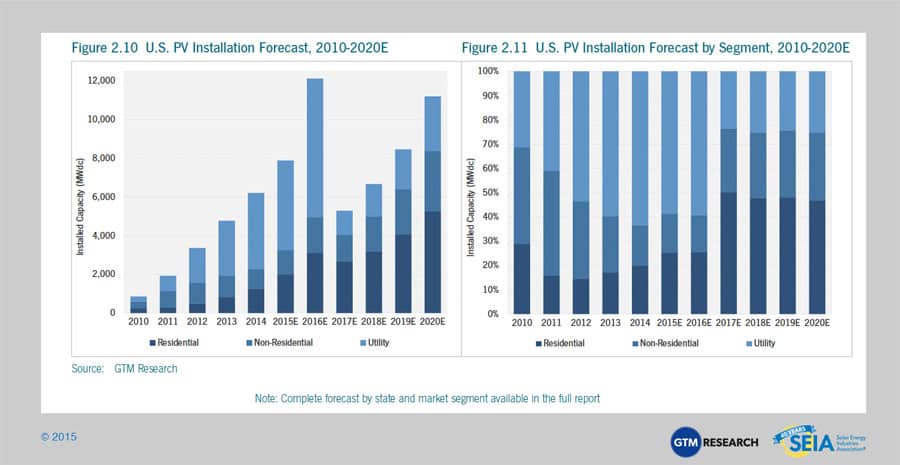

- We forecast that PV installations will reach 7.9 GWdc in 2015, up 27% over 2014. Growth will occur in all segments, but will be most rapid in the residential market.

- 2014 was the largest year ever for concentrating solar power, with 767 MWac brought on-line. The next notable CSP project slated for completion is SolarReserve’s 110 MWac Crescent Dunes, which entered the commissioning phase in 2014 and is expected to become fully operational before the end of 2015.

1. Introduction

Despite a snow-packed winter in the Northeast, the U.S. solar market had a strong first quarter in 2015 with 1,306 MWdc of installations across the country. For a variety of reasons ranging from weather to accounting and tax purposes, Q1 tends to be a slow quarter for solar installations. That was true in both the non-residential and utility solar markets this year, both of which were down quarter-over-quarter from Q4 2014. But the residential market saw no such decline and instead grew 11% over Q4 2014 to have its largest quarter ever.

We anticipate another record year for solar in the U.S. in every market segment. The residential juggernaut will continue to roll on, while the non-residential market will pick up, particularly in California and New York. And the utility-scale pipeline has reached unprecedented levels ahead of the looming federal Investment Tax Credit expiration.

Beyond the numbers, one important trend is rapidly gaining traction throughout the market: technology convergence. Whereas distributed solar has historically been primarily a single offering to customers, solar developers and installers are increasingly seeking opportunities to combine solar with other technologies and services. Among the more prominent adjacent offerings:

- Energy Storage – Distributed energy storage is a nascent but fast-growing sector in the U.S., and it is often a perfect complement to solar. Commercial customers can use energy storage to optimize their solar generation and avoid costly peak demand charges, while residential customers can use energy storage to allow their solar systems to provide backup power in the event of grid outages. Many major solar companies in the U.S. now offer some form of energy storage, particularly in California, Hawaii, Arizona, New York, and Massachusetts. Solar and storage are also often the core elements of microgrids, which are growing throughout the country.

- Load Control – At both the residential and commercial levels, solar is increasingly being offered in combination with electricity load control (or smart home/building) services, which optimize overall electricity consumption and solar generation against customers’ utility tariffs. Many residential solar systems now come with a complimentary smart thermostat or smart home kit, and commercial customers are increasingly seeking combined offerings to ensure maximum savings.

- Demand Response – As with load control, demand response services can often be even more effective when combined with residential or commercial solar. This combination is newer, but a number of companies are testing out combined offerings, including SunPower and EnerNOC.

- Electric-Vehicle Charging – As the electric-vehicle market grows, more and more solar companies are likely to partner with EV charging suppliers on combined services. The two technologies are both complementary from a customer standpoint (there is significant overlap between potential EV owners and solar customers), and ultimately an economic one as EVs become more integrated with the grid.

- This technology convergence is still in its infancy, and the vast majority of solar systems are installed without these ancillary offerings. But as adjacent technologies become more cost-effective, and as electricity rates evolve, we expect to see further convergence and more integrated energy offerings for customers.

2. Photovoltaics

2.1.1 Market Segment Trends

Residential PV

Key Figures:

- Up 11% over Q4 2014

- Up 76% over Q1 2014

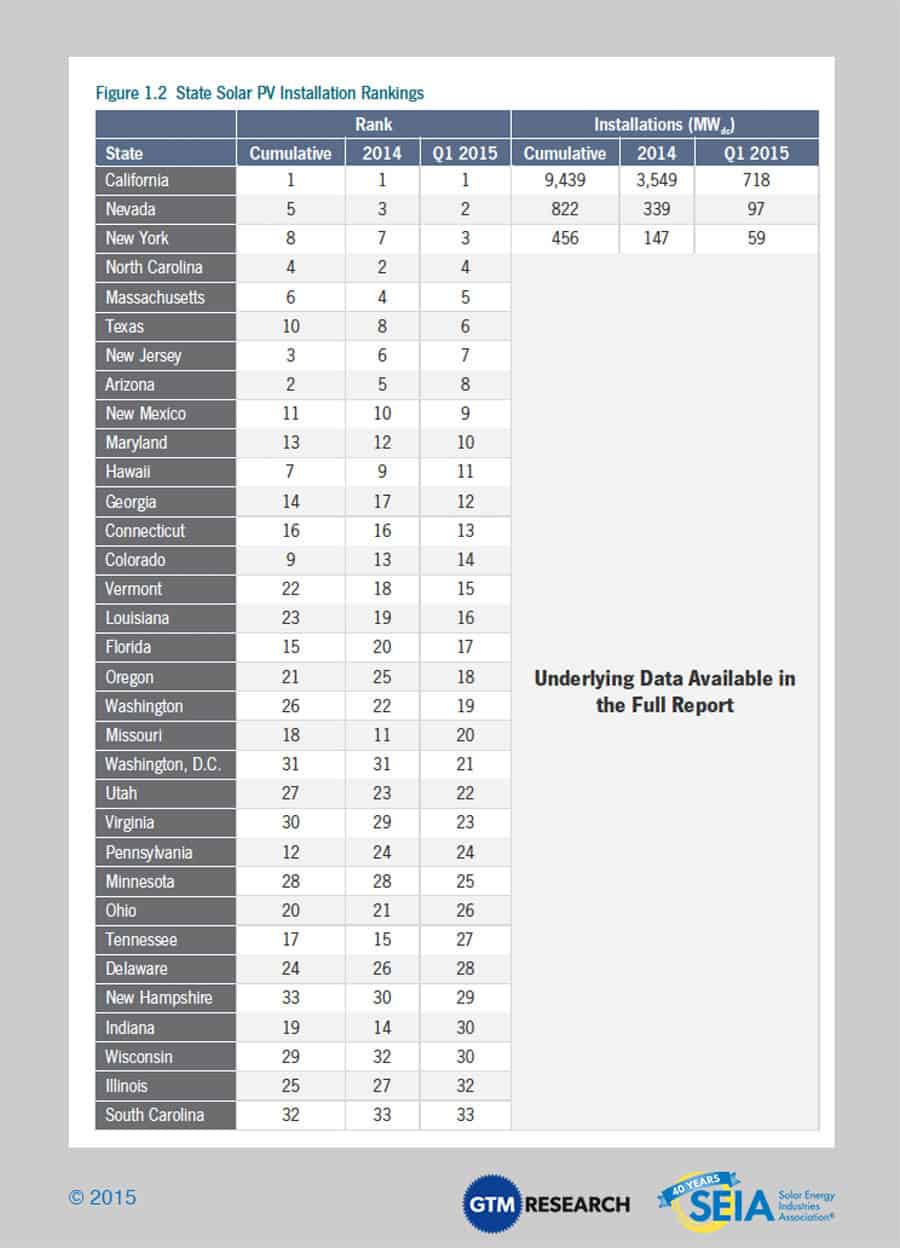

The residential PV market remained strong in Q1 2015, adding more than 400 MWdc on a quarterly basis for the first time ever. While the national residential market grew 11% over Q4 2014, this continued top-level growth remains primarily pegged to demand in California, which drove 53% of national residential installations. However, demand is heating up outside of California, both in select states in the West and in the Northeast. Most notably, New York added 40 MWdc for the second quarter in a row, while Q1 2015 saw Nevada add more residential installations than the state installed throughout all of 2014.

Non-Residential PV

Key Figures:

- Down 24% from Q4 2014

- Down 3% from Q1 2014

The non-residential market continues to struggle from longstanding barriers to customer origination and project finance, and it remains more sensitive to state incentive reductions than residential solar. While the non-residential segment dipped quarter-over-quarter and year-over-year, five of the six largest state markets did grow year-over-year. Most notably, California grew by 45% year-over-year as demand begins to emerge outside of state-incentive-driven opportunities. Overall, however, we remain cautiously optimistic about the non-residential market’s outlook, and expect 21% growth for 2015. As discussed in greater detail within the full report, non-residential solar’s incremental rebound in 2015 is expected to come from three factors: California utilities expanding their solar-friendly tariffs for commercial solar, community solar’s emergence, and corporate procurement of onsite solar.

Utility PV

Key Figures:

- 644 MWdc installed in Q1 2015

- 8th consecutive quarter utility PV added at least half a GWdc

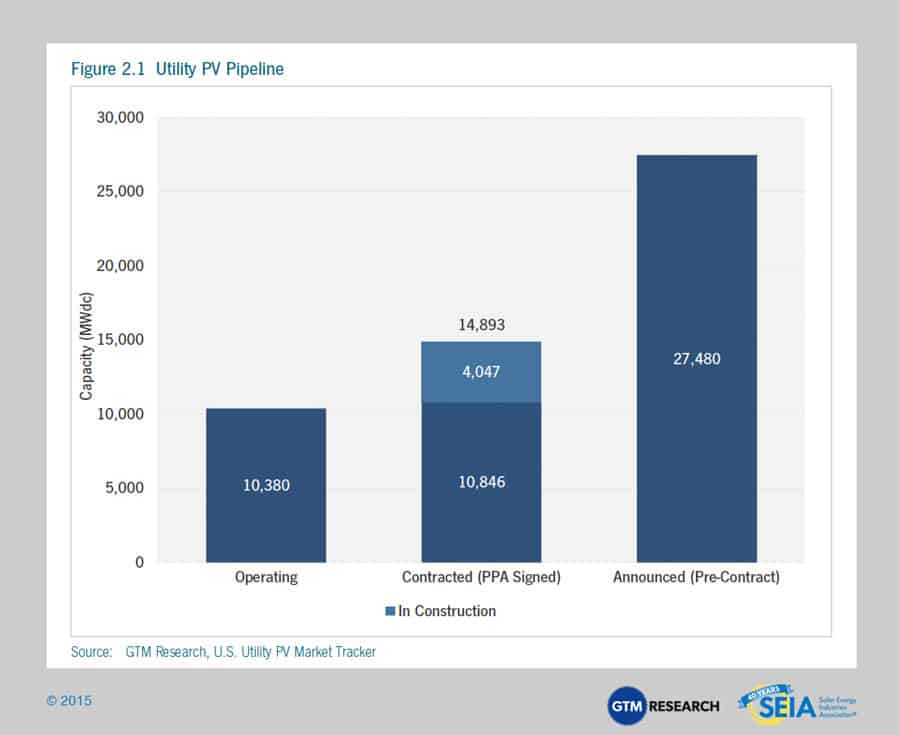

The utility PV sector added fewer installations in Q1 2015 than the segment brought on-line in any quarter last year, yet utility PV still accounted for 49% of new capacity installed across all three market segments. Amidst relatively weak installation volumes, major highlights in Q1 2015 centered on consolidation across the project developer landscape and aggressive procurement of centralized solar by utilities and now corporate entities as well.

New capacity in development outpaced capacity brought on-line in Q1 2015 by approximately 500 MWdc. In turn, there are now 25 developers with pipelines in development of 100 MWdc or more. However, with just over a year and a half until the federal ITC is scheduled to drop from 30% to 10% for the utility PV segment, the timeline to complete these ambitious project pipelines is increasingly tight. An encouraging indicator of utility PV’s aggressive growth trajectory in 2015 and 2016 has been the uptick in construction activity, with total capacity under construction now greater than 4 GWdc for the first time in two years. Throughout 2015, construction activity is poised to outpace project origination as developers maintain a laser focus on ensuring their pipelines achieve commercial operation before the end of 2016.

2.1.2. Full Report Excerpt | Residential Retail Rate Parity: Are We There Yet?

t the end of 2012, only 2% of cumulative residential capacity had come on-line without a state- or utility-level incentive. Fast forward to Q1 2015, and now nearly 25% of cumulative residential capacity has come on-line independent of state incentive funding. This trend of “retail rate parity” is one that has become increasingly prevalent of late—largely because of the growing number of states where residential solar projects are being installed with only net energy metering (NEM), the federal 30% Investment Tax Credit, and in the case of third-party-owned systems, accelerated depreciation.

Markets where utility or state incentives have come and gone, such as in California or Arizona, can provide valuable insight as to the ability of solar projects to pencil out once incentives are out of the picture.

In California, the residential incentives offered by the California Solar Initiative (CSI) are now fully depleted in all three investor-owned utility (IOU) service territories, yet the state’s residential market continues to grow at a record pace. In Q1 2015, 94% of residential installations came on-line across the IOUs without state incentives. Meanwhile, Arizona has become the next major state market to see meaningful residential installation growth without state incentives, following the depletion of upfront residential rebates in APS territory in late 2013 and incentive reductions across other utilities within the state. In Q1 2015, all but 14% of Arizona’s residential installations came on-line without a state incentive.

Unlike California and Arizona, where retail rate parity has unfolded as rebates neared depletion, some state markets with incentive programs, including New York and Nevada, have a minor but growing share of installations coming on-line without the support of state incentives. This trend has been driven largely by installers that forgo rebates in order to execute aggressive growth plans (and avoid sometimes burdensome paperwork), and it further demonstrates that some projects can pencil out without incentives, even when incentives are available.

While state incentive funding has proven less critical in a handful of state markets, the majority of markets across the U.S. still depend on state-level incentive funding to make residential solar economically viable. There are now 14 states where rooftop solar can offer an attractive year 1 discount to a customer’s electricity bill of 10% or greater if third-party owned, or offer a payback period of less than 10 years if directly owned. Although a growing number of states are hitting tipping points in terms of economic attractiveness, it is expected that residential solar will remain primarily driven by the handful of established state markets, especially California, where rate design and net metering rules allow for the highest savings opportunities.

2.2. National Solar PV System Pricing

As was true over the last year of U.S. Solar Market Insight reports, we continue to utilize a bottom-up methodology to capture and report national system pricing. While we continue to solicit weighted average system pricing directly from utility and state incentive programs, we believe that this data no longer accurately reflects the current state of system pricing, as it often represents systems quoted well prior to the installation and connection date, and much of the reported data is based on fair-market-value assessments for TPO systems.

Our bottom-up methodology is based on tracked wholesale pricing of major solar components and data collected from major installers, with national average pricing supplemented by data collected from utility and state programs. While we will no longer be reporting system prices state by state, we will still continue to show reported system pricing from state and utility incentive programs.

Year-over-year, system pricing has fallen by 9% to 14%, with the largest declines in the non-residential sector. Module pricing in the U.S. has remained steady with a year-over-year decline of just 1.4%, meaning that balance-of-system costs have been the root cause of overall system cost declines. Hardware vendors continue to report significant pressure over the past year, although “soft-cost” reductions have remained relatively in step with hardware-cost reductions.

Quarterly trends show a 2% to 3% decline in system prices across market segments, underscoring a continuing incremental stepdown in national system pricing on an aggregate basis. Markets with a large footprint, such as California, continue to have a disproportionate effect on overall national average pricing, which can vary by as much as 20% from state to state. Variations in utility system costs are much smaller than variations in residential and non-residential costs.

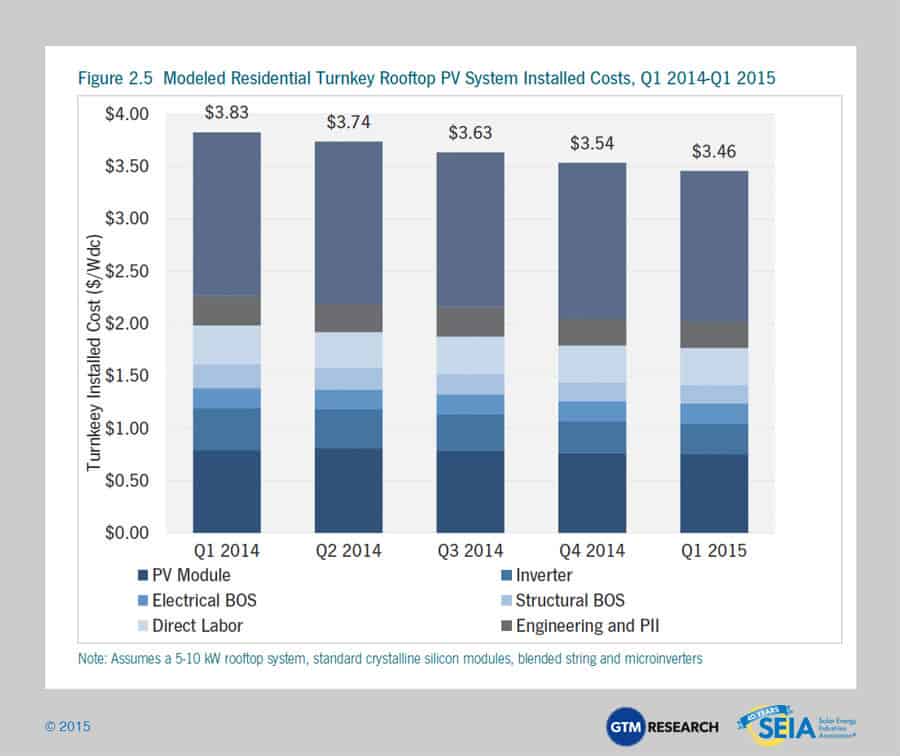

2.2.1. National Residential System Prices

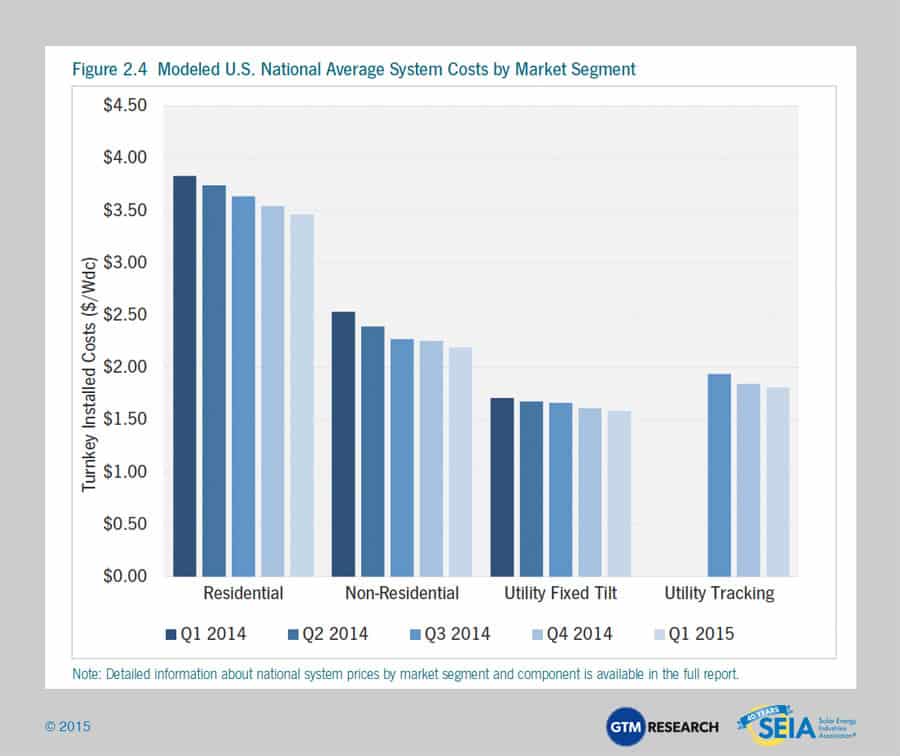

Capacity-weighted average residential system pricing reported by state and utility solar programs for Q1 2015 dropped to $4.43/Wdc, a decline of 4% over Q4 2014 reported prices. We continue to assert that these reported prices conflate numerous pricing definitions. Instead, our bottom-up model points to a turnkey installed cost of $3.46/Wdc in Q1 2015. This reflects a 2.4% reduction to our revised Q4 2014 costs of $3.57/Wdc. This represents a 10% cost reduction over Q1 2014 – an impressive decline considering nearly stagnant module pricing. We also note that reductions in balance-of-systems costs have been split almost evenly between hardware-cost reductions and soft-cost reductions.

2.3. National Non-Residential System Pricing

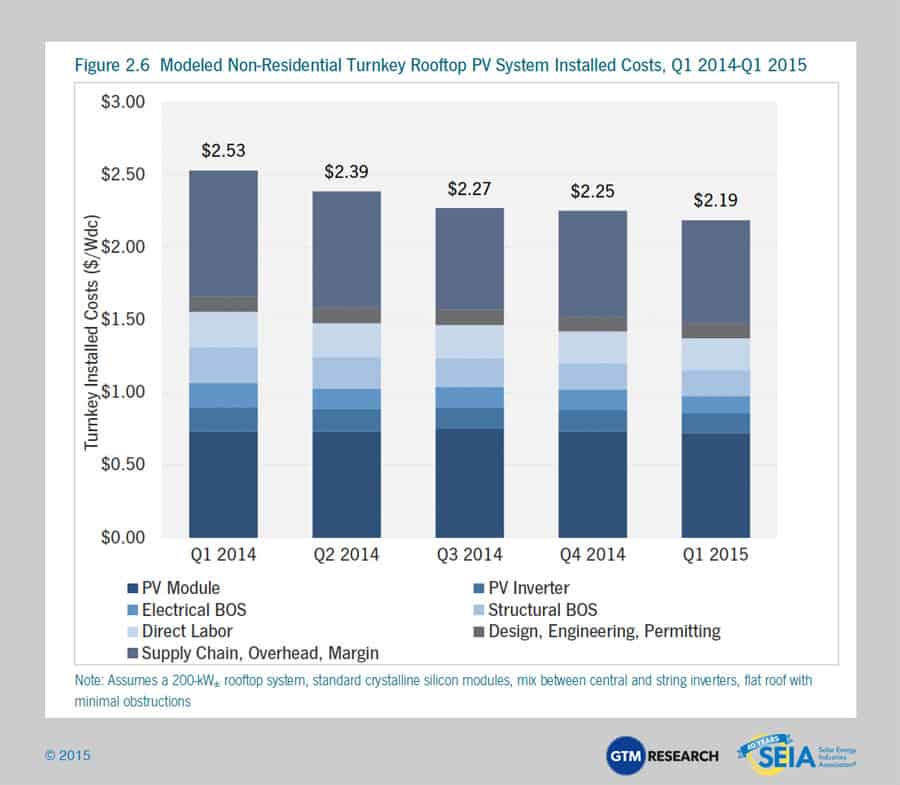

Reported non-residential system costs dropped from $3.43/Wdc in Q4 2014 to $3.23/Wdc in Q1 2015, reflecting a 6% cost reduction. As with reported residential system pricing, this number can be misleading. In addition to the various forms of reporting methodologies, the category “non-residential” tends to capture a grab bag of differing project types, from large commercial ground-mount systems with costs approaching utility systems to small-scale carport projects with cost structures closer to residential systems. Furthermore, “non-residential” also captures projects installed for both private and public organizations, with the latter often incurring additional permitting and overhead costs. As with residential, we work closely with component manufacturers and installers to build a bottom-up model to better reflect typical turnkey installed costs.

We model costs for a medium-scale commercial rooftop system in Q1 2015 at $2.19/Wdc, a 3% decline from Q4 2014. This also represents a 14% decline from $2.53/Wdc modeled for Q1 2014. On the low end, we continue to see larger commercial rooftop projects being built for less than $2.00/Wdc. Smaller-scale commercial project pricing can exceed $3.00/Wdc.

2.4. National Utility System Pricing

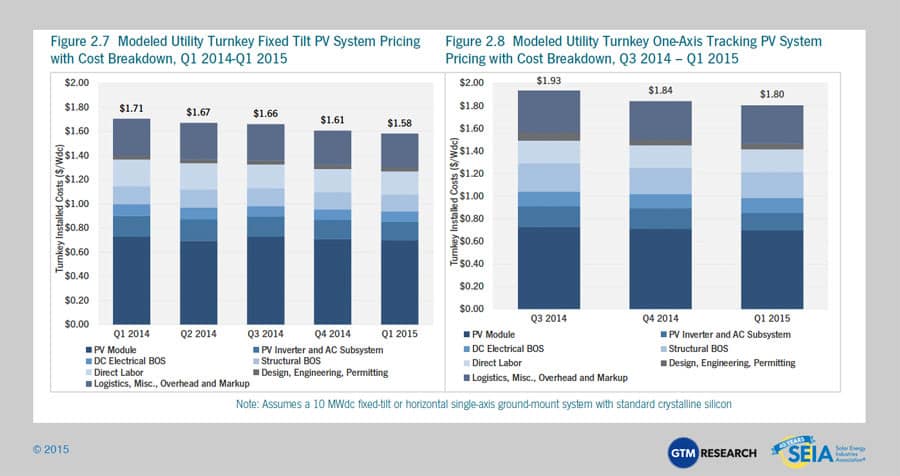

Unlike residential and non-residential systems, utility system pricing is rarely reported. As a result, our national capacity-weighted average incorporates publicly reported pricing where available, as well as input from utility developers and EPCs. National weighted-average system pricing for utility systems in Q1 2015 came in at an average of $1.79/Wdc, a 4% increase from the $1.72 value tracked in Q4 2014. This reported average is more reflective of the types of projects that came on-line in Q1 2015 than it is any indication of increased system pricing. From a bottom-up modeled perspective, we see fixed-tilt projects with installed costs of $1.58/Wdc and tracking projects at $1.80/Wdc. Note that these models assume standard multicrystalline modules, which was not reflective of the bulk of utility PV capacity installed in Q1 2015. Nevertheless, modeled utility project costs dropped 1.5% to 2% in Q1 2015 over Q4 2014.

2.5. Component Pricing

2.5.1. Polysilicon, Wafers, Cells and Modules

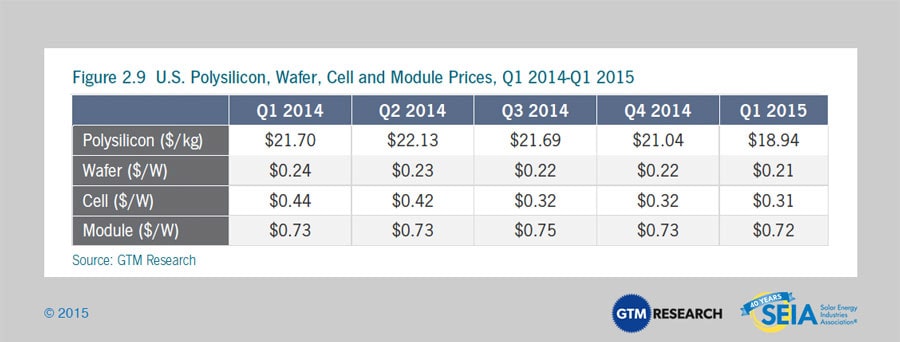

Pricing for polysilicon and PV components fell quarter-over-quarter in the first quarter of 2015. Significant polysilicon price reduction was driven by increased inventory and seasonally weak demand, with prices falling 10% to $18.94/kg. U.S. polysilicon producer REC Silicon claims there are limited volumes available under the Chinese polysilicon processing loophole, leading to increased competition before the loophole closes (estimated August 2015). Similar to polysilicon, weak demand and inventory levels affected wafer and cell prices, each falling 4% to $0.21/W and 3% to $0.31/W, respectively.

It should be noted that following the U.S. imposition of antidumping duties on Taiwanese cells and modules, Chinese producers switched from using Taiwanese cells in U.S.-bound modules to using Chinese cells. Previously, prices for Taiwanese-produced cells were relevant to determining the price for a U.S.-bound Chinese-produced module (Q2 2012-Q3 2014), but prices and tariffs on Chinese-produced cells are now driving module prices.

Module pricing in the U.S. differs widely based on order volume, producer region and individual firm. During the first quarter, delivered prices for Chinese modules ranged from $0.68/W on the low side (corresponding to order volumes greater than 10 MW for less established firms) to $0.75/W on the high side (established, bankable firms, order volumes of less than 1 MW). Blended delivered pricing for Chinese modules is estimated to have dropped to $0.72/W, down 1% from this time one year ago.

2.6. Market Outlook

We expect another record year for the U.S. PV market in 2015, with installations reaching 7.9 GWdc, a 27% increase over 2014. The fastest growth will come from the residential segment, followed by the non-residential segment. Utility PV will grow the slowest compared to 2014, but will still account for well over 50% of all installations brought on-line for the fourth consecutive year.

On January 1, 2017, the 30% federal Investment Tax Credit (ITC) is scheduled to drop to 10% for third party owned residential, non-residential, and utility PV projects under Section 48 of the tax code, while the credit for purchases residential PV under Section 25d is scheduled to expire entirely. Businesses across the solar energy industry have begun preparing for the worst while hoping for the best. In general, solar businesses will try to bring as much capacity on-line as possible before the scheduled stepdown. Solar development will continue, but some markets will fare better than others, and resumption of growth after 2017 will look different from the growth seen over the past eight years. For all market segments, the total addressable market will shrink post-2016, some states will fall off the solar map entirely, and resumption of growth at a national level will be due to several states with strong economics.

he utility-scale market shows the most dramatic drop in 2017, not only because of the challenges posed by the lower ITC, but also because project developers have largely turned their attention to bringing their contracted projects on-line before the end of 2016 in order to capture the full 30% credit. Many of these projects have long-term PPAs that begin in 2017 or later but will sell electricity either through short-term PPAs or on the spot market to bridge the gap between their commercial operation date and the beginning of their long-term PPAs. This pull-in of the utility solar pipeline will make the ITC cliff dramatic. Overall, installations are expected to drop 57% in 2017.

3. Concentrating Solar Power

The final quarter of 2013 kicked off the first wave of mega-scale CSP projects to be completed over the next few years, and Q1 2014 built on that momentum with 517 MWac brought on-line. This included BrightSource Energy’s 392 MWac Ivanpah project and the second and final 125 MWac phase of NextEra’s Genesis solar project. While Q2 2014 and Q3 2014 were dormant for CSP, Abengoa finished commissioning its 250 MWac Mojave Solar project in December 2014. As a result, 2014 ranks as the largest year ever for CSP, with 767 MWac brought on-line. The next notable project slated for completion is SolarReserve’s 110 MWac Crescent Dunes project, which entered the commissioning phase in February 2014 and is now expected to become fully operational before the end of 2015.

In 2016, growth prospects for the CSP market in the U.S. are bleak. On one hand, CSP when paired with storage represents an attractive generation resource for utilities, offering a number of ancillary and resource adequacy benefits. However, due to extensive permitting hurdles that have confronted CSP projects, developers are putting their CSP pipelines on hold given the short window to bring projects on-line before the federal ITC is scheduled to expire at the end of 2016. Most notably, Abengoa’s Palen Solar project, BrightSource’s Hidden Hills project, and SolarReserve’s Rice Solar project are all delayed indefinitely.

Beyond 2016, the outlook for the CSP market will depend on further progress made toward mitigating early-stage development hurdles, lowering hardware costs, and strengthening the ancillary and capacity benefits provided by CSP paired with storage.

Acknowledgments

U.S. Solar Market Insight® is a quarterly publication of GTM Research and the Solar Energy Industries Association (SEIA)®. Each quarter, we collect granular data on the U.S. solar market from nearly 200 utilities, state agencies, installers, and manufacturers. This data provides the backbone of this U.S. Solar Market Insight® report, in which we identify and analyze trends in U.S. solar demand, manufacturing, and pricing by state and market segment. We also use this analysis to look forward and forecast demand over the next five years. All forecasts are from GTM Research; SEIA does not predict future pricing, bid terms, costs, deployment or supply.

References, data, charts or analysis from this executive summary should be attributed to “GTM Research/SEIA: U.S. Solar Market Insight®.”

* Media inquiries should be directed to Mike Munsell ([email protected]) at GTM Research and Ken Johnson ([email protected]) at SEIA.

* All figures are sourced from GTM Research. For more detail on methodology and sources, visit www.gtmresearch.com/solarinsight.

Our coverage in the U.S. Solar Market Insight reports include 30 individual states and Washington, D.C. However, the national totals reported include all 50 states, Washington, D.C., and Puerto Rico.

Detailed data and forecasts for all 30 states are contained within the full version of this report, available at www.greentechmedia.com/research/ussmi.

AUTHORS

GTM Research

SEIA