US Solar Market Insight 2010 Q2 & Q3

Introduction

The U.S. solar market is increasingly becoming a central focus of global industry attention, but state-by-state differences in regulations, incentives, utilities, and financing structures introduce more complexities in comparison to other markets. As a result, it has long been difficult to track and understand the changing market dynamics for solar energy in the U.S.

The SEIA/GTM Research U.S. Solar Market InsightTM is our answer to this problem. Each quarter, we survey installers, manufacturers, utilities, and state agencies to collect granular data on photovoltaics (PV), concentrating solar power (CSP), and solar heating & cooling (SHC). This data provides the backbone of Solar Market InsightTM, in which we identify and analyze trends in U.S. solar demand, manufacturing, and pricing by state and market segment. We also use this analysis to look forward and forecast demand over the next five years. As the U.S. solar market expands, we hope that Solar Market InsightTM will provide an invaluable decision-making tool for installers, suppliers, policymakers and advocates alike.

Photovoltaics (PV)

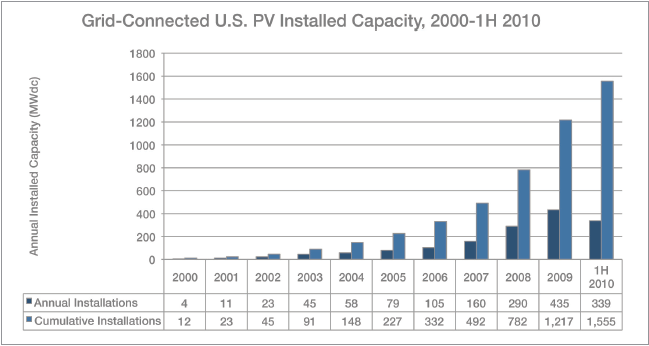

The U.S. PV market has grown at an average annual rate of 69% over the past ten years, rising from just 3.9 megawatts (MW) in 2000 to 435 MW in 2009. Despite this trend, the U.S. constituted only 6.5% of global PV demand in 2009, placing fourth in national installations behind Germany, Italy, and Japan. However, with continued pricing reductions and strong incentives the U.S. could become the next major PV growth market.

Installations (Q2)

The United States is on track to experience a record year for PV installations in 2010. In the first half of the year 339 MW of grid-connected PV were installed. On an annual basis, this represents 55% growth over the 435 MW installed in 2009. Many factors contributed to this growth, including a drastic decline in 2009 module prices, continued federal support from the Section 1603 Treasury Cash Grant in Lieu of Investment Tax Credit program, and expanding state-level targets for solar power.

Read the full report here.

Installations (Q3)

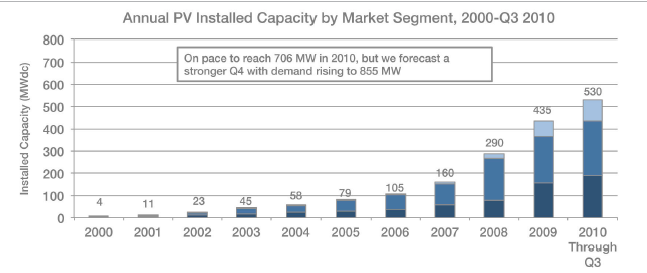

As of the end of the third quarter, the U.S. had already achieved a record year for PV installations. 188 MW were installed in the third quarter, resulting in a total of 530 MW for the year to date. Already, this represents 22% growth over the 435 MW installed in 2009–and the fourth quarter will only add to this total. At a broad level, demand remains driven by the Section 1603 Treasury Cash Grant program, state-level incentives, and improved project economics following a 2009 module price crash amidst the global financial crisis.

Read the full report here.