US Solar Market Insight Q3 2011

Introduction

Through the third quarter of 2011, the U.S. solar market installed more than 1 gigawatt (GW) of grid-connected photovoltaics (PV) on the year, far surpassing the 2010 annual total of 887 megawatts (MW). The third quarter of 2011 was also the largest quarter for installations ever seen in the U.S., supported by utility-scale project completions and rapidly declining prices for PV modules.

Module prices have plummeted due to massive oversupply on a global scale. This is a result of tepid demand in leading European markets combined with substantial manufacturing capacity expansions. While this has been a boon for domestic installations, it has also resulted in an extraordinarily difficult year for PV manufacturers worldwide.

In addition to uncertainty surrounding module pricing, the 1603 Treasury Program is scheduled to expire at the end of the year. Unless the program is extended, we anticipate a tax-equity bottleneck in 2012, stifling some large-scale utility, commercial, and third-party owned residential projects.

In short, the U.S. PV market continues to boom, but considerable risks lie ahead. This report captures and analyzes trends in the U.S. solar market and seeks to demystify the current landscape for U.S. solar installations.

Installations

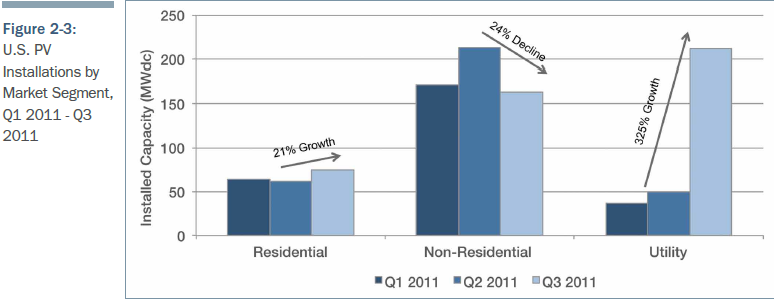

The U.S. installed 449.2 MW in Q3 2011, up 39% over Q2 2011 and 140% over Q3 2010. This makes Q3 2011 the largest quarter in the history of the U.S. PV market, surpassing Q4 2010 by nearly 90 MW. Still, growth across market segments was anything but uniform. While the utility market installed more than ever before, the residential market grew incrementally and the non-residential market shrank to the lowest level since 2010.

Today, the U.S. market faces more uncertainty than at any time in recent history. On one hand, module prices are falling precipitously and system prices have never been lower. On the other hand, the market faces substantial risks in the form of legislative, financing, political, and market barriers. We identify three key questions facing the market:

1. With major markets trending downward, how much can emerging state markets ramp up? The commercial markets in California, New Jersey, and Pennsylvania shrank in Q3, and our expectation is that the trend will continue at least through Q4 (and likely longer in New Jersey and Pennsylvania). Given that those states comprised well over 50% of installations in the first half of the year, overall market growth will necessitate substantial demand pick-up across a number of secondary states. In particular, we are closely watching trends in Massachusetts, Colorado, Ohio, Tennessee, and Hawaii – all of which could be near-term growth markets.

2. What will be the impact of potential 1603 cash grant expiration? As the year-end 2011 expiration date of the Section 1603 Treasury Program approaches, its impact remains somewhat undefined. Assuming no extension, the standard line of reasoning would suggest that the impact will be threefold. First, shipments into the U.S. will jump in Q4 2011 as a result of developers hoping to qualify for the 5% safe harbor provision. Second, installations in Q1 and Q2 2012 will also be propped up as those safe-harbored projects reach completion. Third, the market will ultimately face a tax equity bottleneck in 2012 for new projects, and a slowdown in installations could be felt as early as Q3 2012 for commercial projects and into 2013 for utility projects.

3. How will the trade petition impact market dynamics, both in the immediate term and if duties are ultimately imposed? Adding to the uncertainty already facing the U.S. market, there is the potential imposition of import duties on PV cells and modules originating in China. To briefly recap the issue: SolarWorld Americas, Inc. and six other unnamed petitioners, representing the newly formed Coalition for American Solar Manufacturing (CASM), filed a petition with the U.S. International Trade Commission and the Department of Commerce on October 19, 2011. The petition alleges that Chinese manufacturers of crystalline silicon photovoltaic cells have benefitted from unfair government subsidies and that they have been “dumping” product into the U.S. market. It asks for the imposition of import duties of 100% or more on the wholesale cost of Chinese cells and modules. There are two questions to be asked here in relation to both the upstream and downstream segments of the U.S. solar market: one, what will be the near-term impact as the process plays out, and two, what would be the longer-term impact if tariffs are ultimately imposed? Additional detail surrounding the trade case is available in the full report.

Read the full report here.