U.S. Solar Market Insight Report 2011 Year-in-Review

U.S. Solar Market Insight Report 2011 Year-In-Review

U.S. Solar Market InsightTM is a quarterly publication of the Solar Energy Industries Association (SEIA)® and GTM Research. Each quarter, we survey nearly 200 installers, manufacturers, utilities, and state agencies to collect granular data on photovoltaic (PV) and concentrating solar. These data serve as the backbone of this Solar Market Insight® report, in which we identify and analyze trends in U.S. solar demand, manufacturing, and pricing by state and market segment. We also use this analysis to look forward and forecast demand over the next five years. As the domestic solar industry expands, U.S. Solar Market Insight® will provide an invaluable decision-making tool for installers, suppliers, investors, policymakers and advocates alike.

KEY FINDINGS

Photovoltaics (PV)

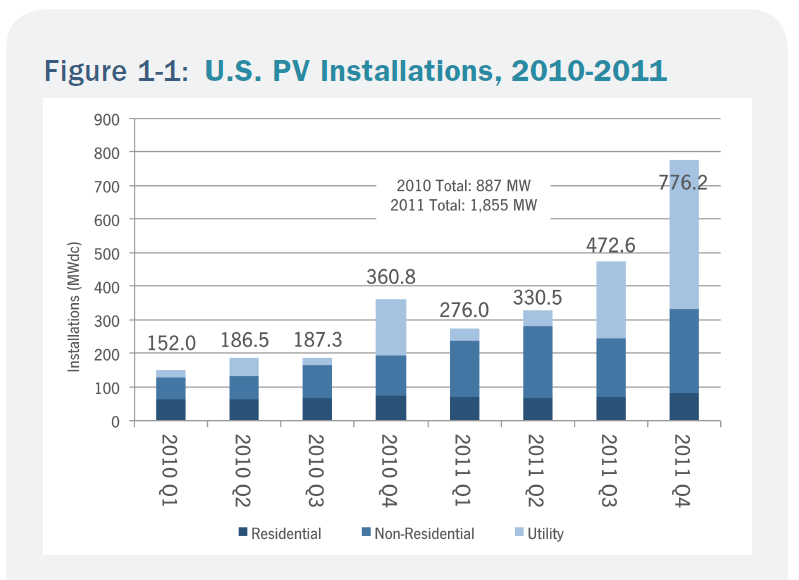

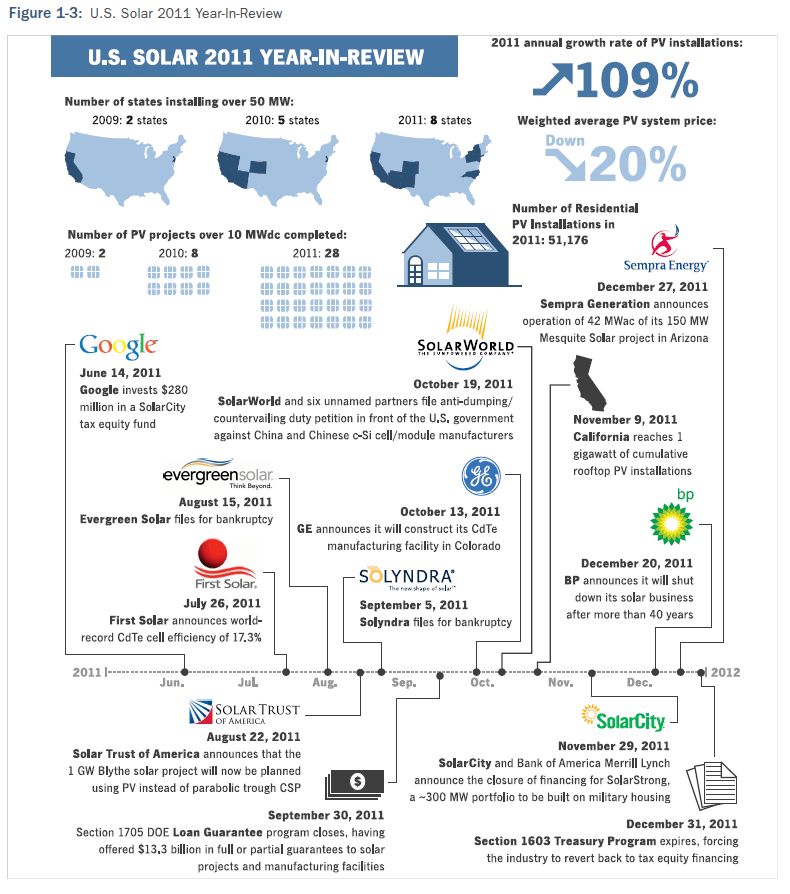

- PV installations grew 109% in 2011 to reach 1,855 MW, which represents 7.0% of all PV globally, up from 887 MW and 5.0% of global installations in 2010.

- Cumulative PV capacity operating in the U.S. now stands at 3,954 MW.

- There were 28 individual PV projects over 10 MW each completed in 2011, up from only two in 2009.

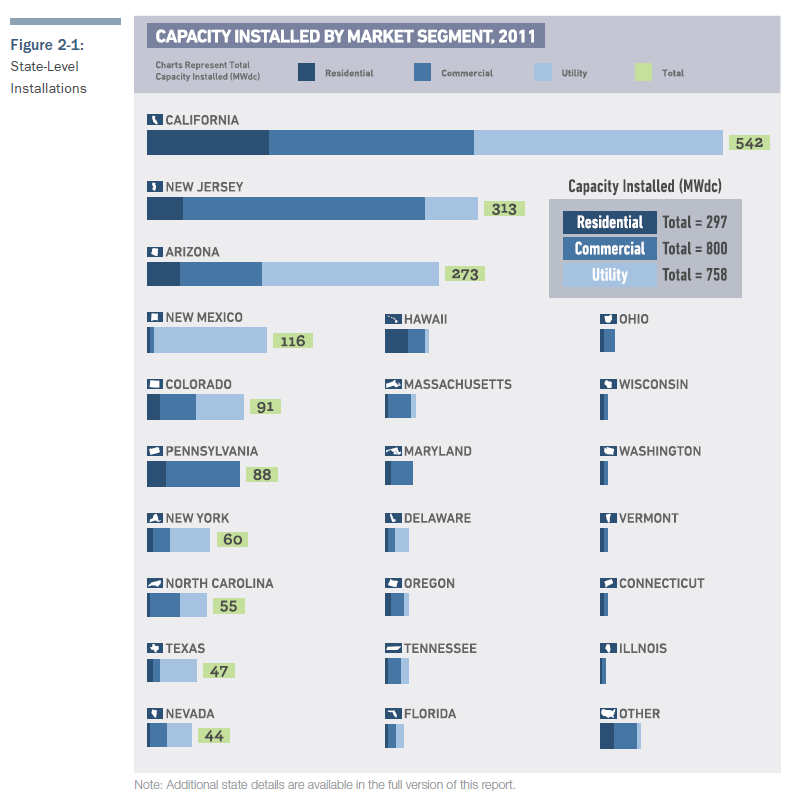

- Eight states installed over 50 MW each in 2011.

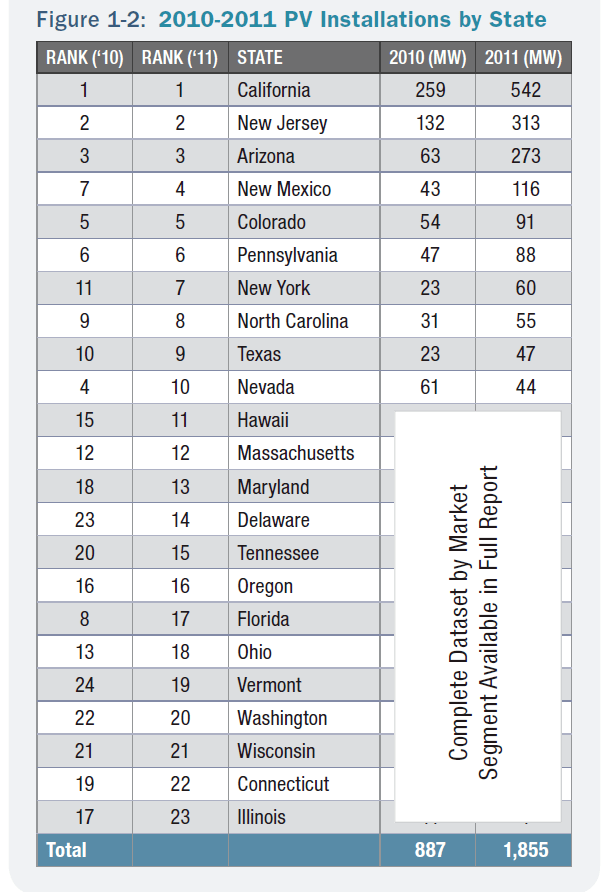

- Installation totals in 2011 increased in 18 of the 23 states we cover in detail.

- Weighted average PV system prices fell 20% in 2011 as a combined result of lower component prices, improved installation effi ciency, and a shift toward larger systems.

- There were over 61,000 individual PV systems installed in the U.S. in 2011, bringing the total number of operating systems in the U.S. to more than 214,000.

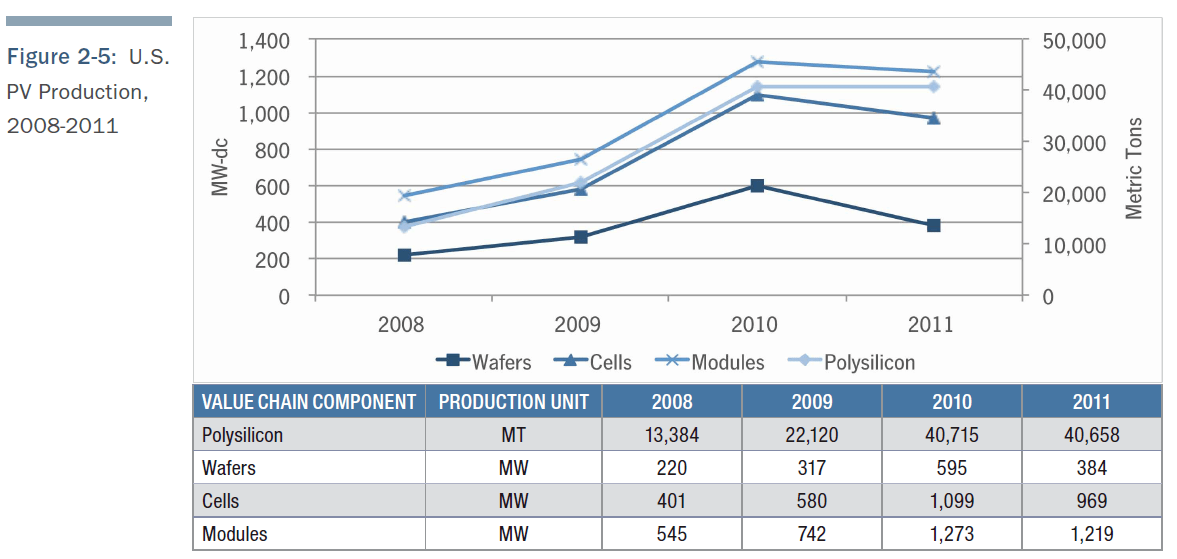

- In total, the U.S. produced 40,658 metric tons (MT) of polysilicon, 384 MW of wafers, 969 MW of cells, and 1,219 MW of modules in 2011; in sharp contrast to 2010, which saw 100% growth in production across the PV value chain, 2011 saw production stay mostly fl at for polysilicon and modules, and shrink signifi cantly in the case of wafers and cells.

- Blended average Q4 2011 prices for polysilicon stood at $43/kg, while blended prices for wafers, cells, and modules were $0.40/W, $0.65/W, and $1.15/W, respectively. Prices for polysilicon and modules experienced drops of 37% and 40%, respectively, from Q4 2010 to Q4 2011. Price drops for wafers and cells over the same period were even steeper, at 62% and 60%, respectively.

- Overall, the value of systems installed in the U.S. in 2011 climbed to $8.4 billion, up from $5 billion in 2010.

Concentrating Solar Power (CSP and CPV)

- Construction on the 30 MW Alamosa CPV plant began in the first half of 2011.

- Financing was secured in Q3 for four concentrating solar projects representing over 600 MW of capacity.

- PPAs were approved in Q4 for over 400 MW of concentrating solar projects.

- Over 1,000 MW of concentrating solar projects are under construction as of December 31st, 2011.

- As of December 31st, 2011, there was a total of 516 MW of concentrating solar capacity operating in the U.S.

INTRODUCTION

For the U.S. solar energy industry, 2011 was a historic year. On the positive side, the market for solar installations continued to boom, as the U.S. installed 1,855 megawatts (MW) of photovoltaic (PV) solar systems, representing 109% growth over 2010. The fourth quarter of 2011 saw 776 MW of PV installed, by far the most of any quarter in U.S. market history (473 MW was the previous record, set in the third quarter of 2011). Growth occurred in every market segment - residential, non-residential and utility - and in 18 of the 23 states that are tracked individually. The dollar amount of project fi nance investments reached an all-time high and traditional energy companies such as MidAmerican Energy Holdings, Exelon and NRG Energy became equity investors in the largest planned solar projects in the country.

Not all developments in 2011 were positive. With regard to installations, the highly valued 1603 Treasury Program expired at the end of the year, subsequently complicating the fi nancing of many new solar projects. As for manufacturing, though global PV module capacity grew more than 50% in 2011, throughout most of the year global demand remained slow as a result of regulatory changes in Italy and tepid growth in Germany. Solar panel prices went into free-fall in the second quarter and refused to stabilize until the last weeks of 2011, ultimately falling more than 50% during the year. This squeezed profi t margins for every manufacturer, but it was particularly damaging for two types of companies: those that were less cost-competitive and those that were in the process of commercializing new technologies. As a result, multiple U.S. module manufacturing plants closed over the course of 2011. Despite these closures, U.S. module manufacturing capacity expanded 28% and production remained fl at for the year when compared to 2010.

In the wake of precipitously falling module prices, SolarWorld, along with six unnamed partners, filed an anti-dumping/countervailing duty petition against Chinese crystalline silicon cell and module manufacturers with the Department of Commerce and the International Trade Commission in October 2011. The petition alleges that Chinese suppliers benefi tted from illegal subsidies and dumped product into the U.S. market. The outcome of the petition remains to be seen. However, it has already begun to impact procurement patterns and complicate the overall supply picture in the U.S.

In September 2011, Solyndra, a CIGS module manufacturer, fi led for bankruptcy and brought with it a storm of negative attention to the solar industry. While Solyndra was never a significant player in the global solar industry, its default on a federal loan guarantee brought a high-profile political element that was absent for the other two U.S. solar bankruptcies in 2011 (Spectrawatt and Evergreen Solar). As a result, an industry blessed with overwhelming public support suddenly became a target for those who sought to admonish the loan guarantee program or clean energy policy in general.

While it is easy to brush aside the more outlandish claims made in response to Solyndra's failure regarding solar technology in general, the Solyndra story has brought a number of valuable questions to the forefront. First, has the support that has been given to the solar industry, both at the state and federal level, been successful? The market's impressive recent growth points to yes. Installations are booming, jobs are being added, and solar has proven itself as a reliable technology to meet growing energy demand. Second, is there a role for U.S. solar manufacturing? Here, there is reasonable debate on both sides.

We continue to believe that the U.S. can maintain a presence in manufacturing innovative, proprietary technologies, particularly those in their early stages of commercialization. Apart from this, the U.S. can remain home to the bulk of innovations that drive down the cost of solar power for years to come. That being said, it would be unreasonable to expect all (or even most) solar manufacturing to come from the U.S. The solar industry is global, and consequently subject to the same economic forces as manufacturing in other sectors. Undoubtedly, some portions of the value chain will fi nd domestic manufacturing attractive while others will not. The U.S. certainly has a role to play, but it will be over the next decade that the nature of that role will be determined. As the industry continues to mature, successful and sustainable companies will be separated from hopeful but ultimately unsuccessful ventures.

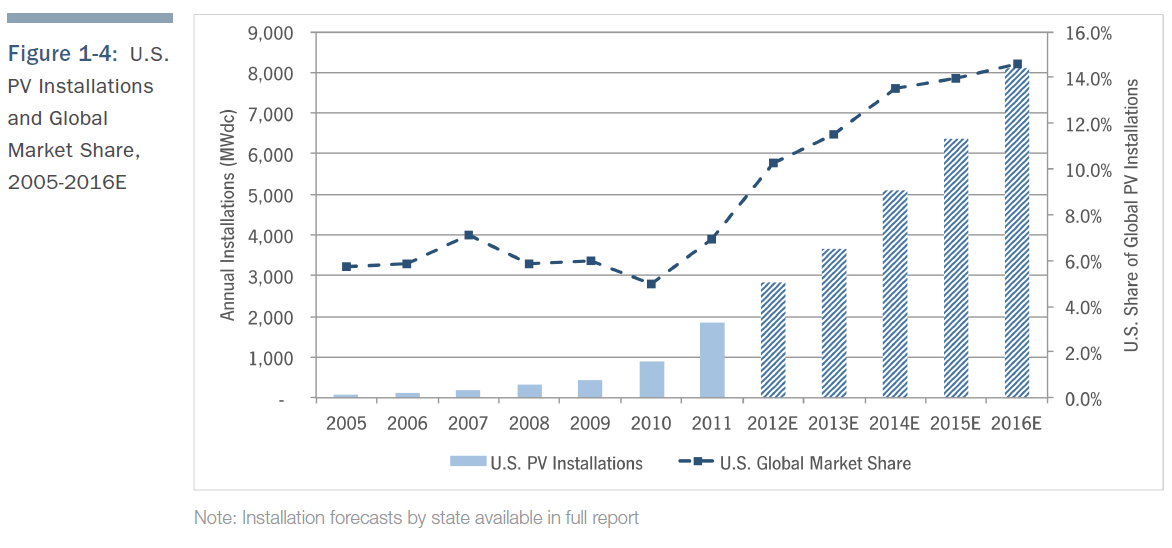

After a recording-breaking 2011, the U.S. has proved itself as a viable market for solar on a global scale. In 2011, the U.S. market's share of global PV installations rose from 5% to 7% and should continue to grow. We forecast U.S. market share to increase steadily over the next five years, ultimately reaching nearly 15% in 2016 – at which point we anticipate the U.S. and China to be the leading markets in the world as European markets slow down. Given that solar installations in the U.S. have more than doubled in each of the past two years, and that the current project pipeline far exceeds current installation levels, this is a highly probable outcome.

PHOTOVOLTAICS

Photovoltaics (PV), which convert sunlight directly to electricity, continue to be the largest component of solar market growth in the U.S.

PV INSTALLATIONS

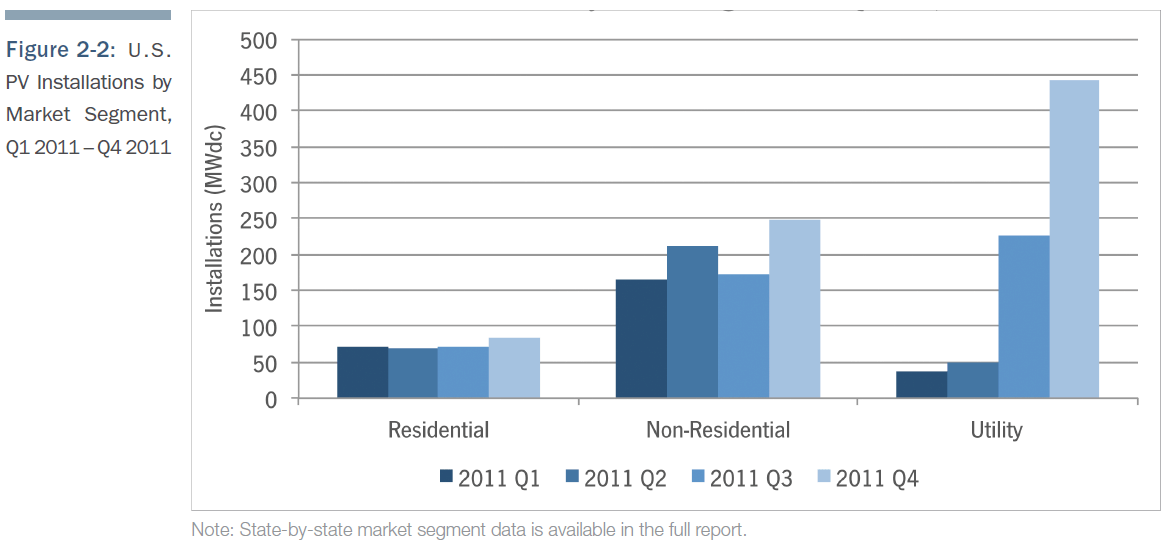

The U.S. installed 776 MW in Q4 2011, up 64% over Q3 2011 and up 115% over Q4 2010. Every market segment had a record quarter, as did ten individual states. Three factors were primary contributors to the quarter's impressive growth figures:

- Seasonality - The fourth quarter is usually the strongest in the U.S. as developers rush to finish projects for tax accounting purposes and to qualify for incentives that function on a calendar year.

- Looming Expiration of the Section 1603 Treasury Program - As was true in 2010, most installers were working under the assumption that Section 1603 would not be extended. Although we expect that more developers elected to safe-harbor product in 2011 (which enabled projects completed after the December 31st, 2011 deadline to qualify for the program), many projects were still completed in Q4 in order to eliminate the risk and transaction costs of safe harboring.

- Utility Project Completions - There were over 400 MW of utility PV completed in Q4 2011, by far the highest of any quarter for this market segment.

For the last several years, the U.S. market has been driven primarily by the non-residential sector, which accounted for more than 50% of installations through 2008. However, the utility sector has been gaining ground, while the residential market has remained relatively steady. In 2011, the dynamic amongst market segments shifted substantially throughout the year, but the overall trend has been toward the growth of the utility market. Meanwhile, the residential market showed marginal overall growth.

The largest of the three, the non-residential market, which is dominated by commercial installations, was heavily dependent on statelevel dynamics in California and New Jersey. The utility market, however, showed sustained growth for the first time, with 28 projects over 10 MW installed in 2011 - up from just two in 2009.

- Residential installations grew 11% in 2011 over 2010 to reach 297 MW. California was the primary driver of this growth, particularly in the fourth quarter. Within California and in an increasing number of other states, residential growth has been driven primarily through third-party ownership. In Q4 2011, for the first time, more third-party-owned systems were installed in California Solar Initiative territory than customer-owned systems. And over the past two years, while customer-owned systems have largely stagnated, third-party ownership sales continue to grow.

- Non-residential installations grew 127% in 2011 to reach 800 MW. In large part, this growth was due to two states, California and New Jersey, which contributed 56% of the national non-residential installed capacity in the fourth quarter. Both of these states should also show strong installations numbers early in 2012, but could taper off somewhat in Q2/Q3. While a number of other markets should see growth (Massachusetts, Maryland, North Carolina, Arizona), national fi gures will still be heavily dependent on the two largest states.

- Utility installations grew 185% in 2011 to reach 758 MW, by far the largest growth of any segment. Growth prospects for the utility market remain strong. There are over 9 GW of projects with signed utility power purchase agreements (PPAs) awaiting completion over the next fi ve years. Over 3 GW of these projects have already been financed and are in construction. Beyond this, there are at least 30 GW of earlier-stage projects actively seeking permits, interconnection agreements, PPAs, and financing.

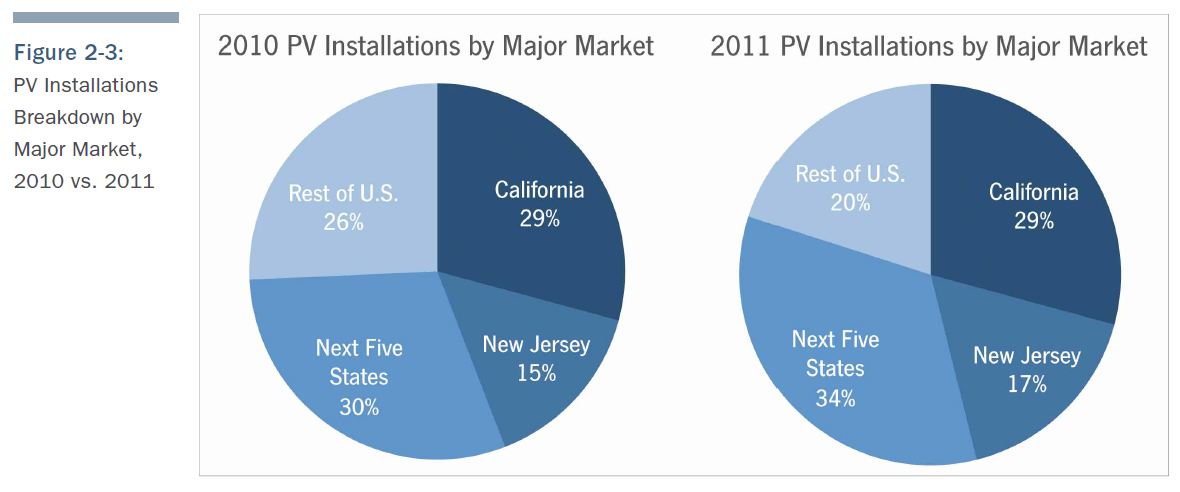

The U.S. PV market remains relatively concentrated in a few key states, although the market has been experiencing rapid geographic expansion over the past few years. Whereas California accounted for around 80% of total installations in 2004-2005, by 2010 it made up less than 30% of the national market. In 2011, California's market share remained remarkably steady at 29%. The next six states, however, grew to encompass 51% of the national market, up from 45% in 2010. In other words, while the market is shifting away from California alone, it is still concentrated in a relatively small set of secondary markets as opposed to full diversifi cation across the U.S. In 2012, given the potential diffi culties in major markets such as New Jersey and Colorado, the "Rest of U.S." category may have an opportunity to quickly increase its market share.

INSTALLED PRICE

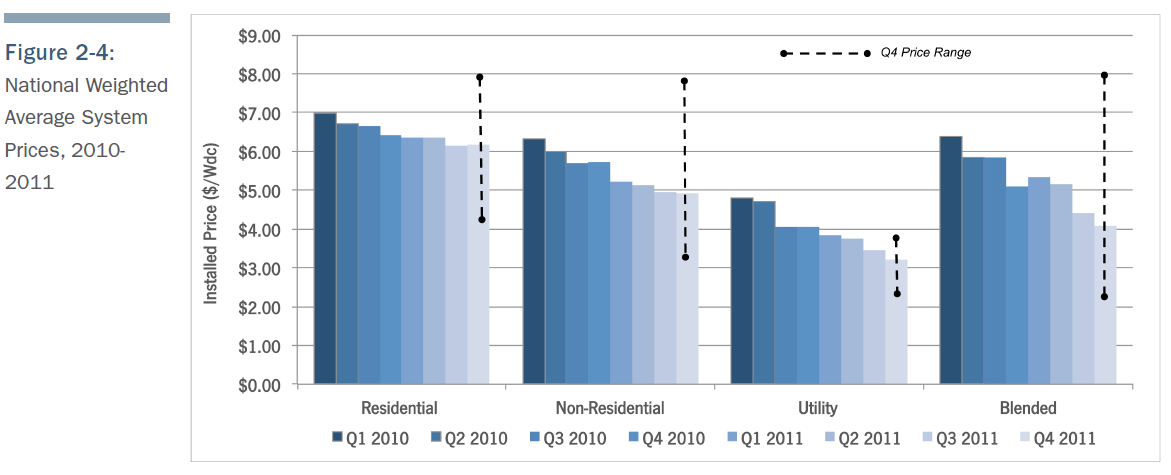

Quarter-over-quarter, the national weighted-average installed system price in the U.S. fell by 7.5% between Q3 2011 and Q4 2011, from $4.41/W to $4.08/W. Year-over-year, average installed costs declined by 20%. This average number is heavily impacted by the large volume of utility-scale and megawatt-plus commercial systems installed in Q4 2011. It should be noted that prices reported in this section are weighted averages based on all systems that were completed in Q4 in many locations.

- Residential system prices increased by 0.7% from Q3 2011 to Q4 2011, as the national average installed rose slightly from $6.14/W to $6.18/W. Year-over-year, installed costs declined by 3.6%. This quarterly increase is largely a result of relatively small price reductions in the major state markets of California and New Jersey while many secondary, high-cost markets grew in the fourth quarter. With a glut of cheap panels still flooding the market, it was not uncommon to find direct-owned residential systems being installed for less than $5.00/W in larger markets. However, low module prices were counteracted by an uptick in thirdparty-owned systems as these installations are reported as costing more than direct-owned systems.

- Non-Residential system prices fell by just 0.4% quarter-over-quarter, moving from $4.94/W to $4.92/W. Year-over-year, installed costs declined by 13.9%. Higher average prices in Arizona, which had a large amount of non-residential capacity installed in Q4, negated lower costs in New Jersey and Hawaii, which also had impressive quarters. California saw almost no change. As in Q3, aggressive bidding was a major factor in lower prices in the East Coast markets. With SREC prices continuing to fall, developers are constantly bidding lower to keep projects attractive to investors. For larger, well-established installers and integrators, buying significant quantities of modules on the spot market or via short-term supply agreements helped them leverage low prices during the Q4 installation rush.

- Utility system prices declined for the seventh consecutive quarter in a row, dropping from $3.45/W in Q3 2011 to $3.20/W in Q4 2011. Year-over-year, installed costs declined by 21%. This 7.2% reduction in costs is a direct result of a historic free-fall in the global price of solar modules, especially when purchased in large quantities. A number of large projects, including a few 20 MW-plus installations, came on-line in Q4, which further emphasized economies of scale and drove the average installed price to its lowest point in the history of the U.S. Solar Market Insight reports.

MANUFACTURING

In total, the U.S. produced 40,658 MT of polysilicon, 384 MW of wafers, 969 MW of cells, 1,219 MW of modules and 1,653 MW of inverters in 2011. In sharp contrast to 2010, which saw 100% growth in production across the PV value chain, 2011 saw production stay mostly fl at for polysilicon and modules, and shrink significantly in the case of wafers and cells. As shown in Figure 2-5, these relatively disappointing results come after a sustained period of robust growth for the domestic manufacturing industry.

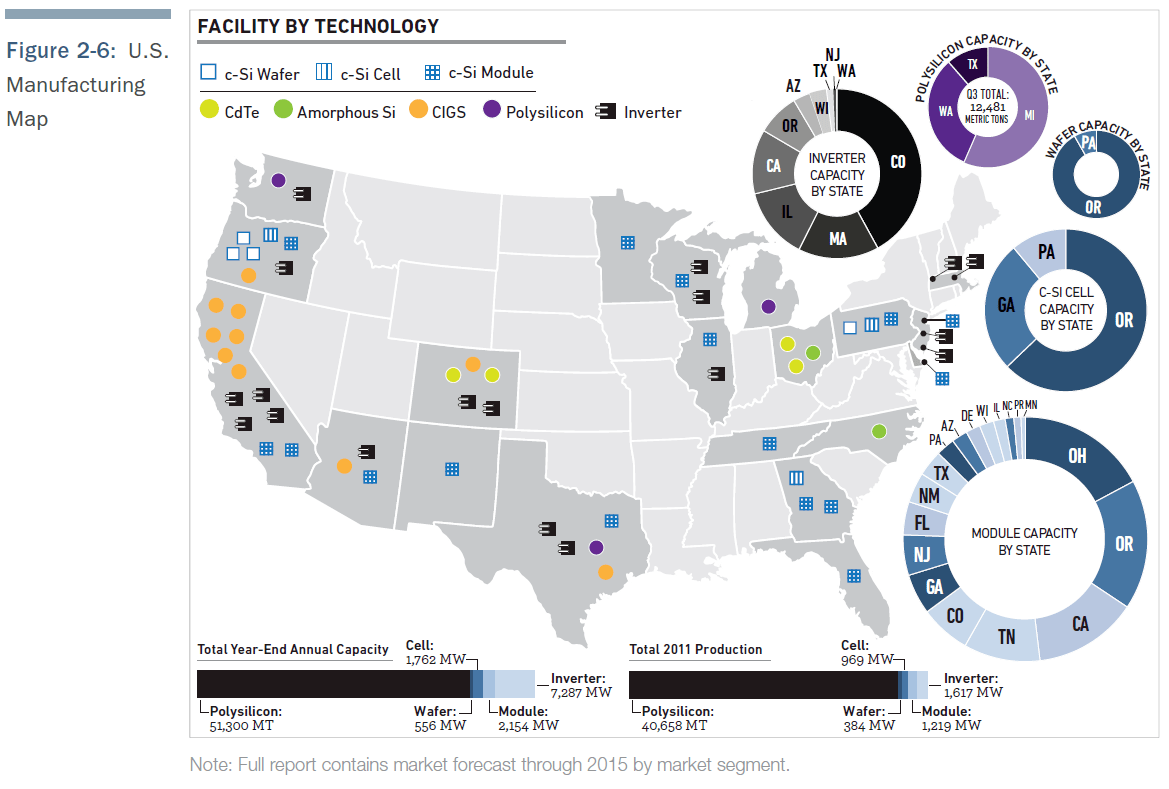

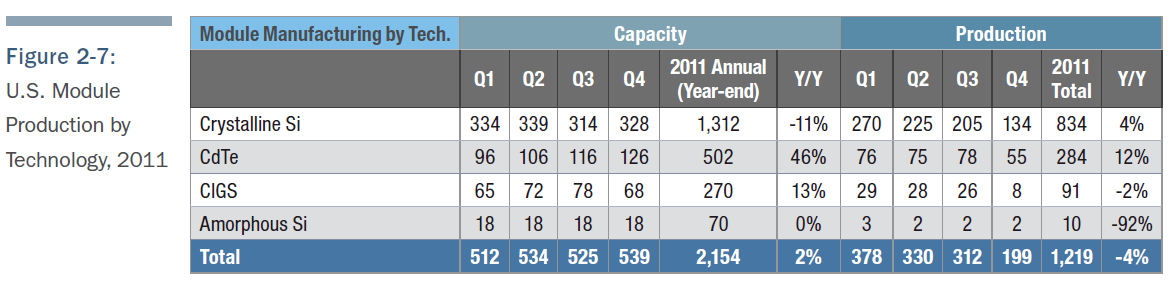

In terms of technology trends, the dominant majority of modules produced in the U.S. in 2011 were crystalline silicon (68%) and cadmium telluride (23%), with small amounts of CIGS (7%) and amorphous Si (1%). Overall U.S. thin fi lm production share stood at 32%, but this is expected to increase over the course of 2012 and 2013 as numerous thin fi lm facilities come on-line and ramp up production. Thin fi lm facilities tend to be located in close proximity to R&D resources, given their technology-intensive nature. This explains the high concentration of thin fi lm plants in California (Silicon Valley) and Colorado (NREL), and is part of the reason why the concentration of thin fi lm of production in the U.S. greatly exceeds its share globally.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

MARKET OUTLOOK

U.S. market prospects are generally strong. This quarter we have increased our base case 2012 forecast from 2.5 GW to 2.8 GW as a result of the large quantity of product safe harbored to meet the Section 1603 Treasury program year-end deadline. Most of these projects will be completed in 2012 and will prop up installation totals throughout the year. In addition, we are more bullish on near-term growth prospects in the California commercial market and in the prospects for many of the utility-scale projects in the pipeline to attain fi nancing. In truth, 2012 market size will still be largely determined by factors that have not yet been decided, such as the fi nal outcome of the trade petition and market dynamics in Germany and Italy.

CONCENTRATING SOLAR

INSTALLATIONS

Ten concentrating photovoltaics (CPV) projects were completed in 2011. The majority of this capacity came on-line in Q2 2011, with only two projects interconnected in Q4 2011. There were no concentrating solar power (CSP) projects completed in 2011, though a number of large projects are currently under construction and slated for commissioning in the next two years. While total capacity installed in 2011 was lower than originally expected, there was additional progress on several of the large concentrating solar projects under development.

Significant developments in 2011 include:

- The DOE finalized a $1.6 billion loan guarantee for the 370 MW (net) Ivanpah plant.

- The 484 MW Blythe Phase I plant was offered a conditional $2.1 billion loan guarantee and subsequently switched from trough to PV.

- Solar Trust of America sold its 2.25 GW, four-project CSP pipeline to Solarhybrid, which plans to use PV for the four projects.

- Several concentrating solar projects closed DOE loan guarantees in Q3 including:

- 250 MW Mojave Solar trough CSP project

- 110 MW Crescent Dunes tower CSP project

- 250 MW Genesis trough CSP project

- 30 MW Alamosa CPV project

- Over 400 MWac of concentrating solar power purchase agreements were approved by the California Public Utilities Commission in Q4, including:

- 250 MW Mojave Solar trough CSP project

- 5 MW Littlerock CPV project

- 4.8 MW Garnet CPV project

- 4.7 MW Blythe CPV project

- 14 MW Lucerne Valley CPV project

- 80 MW Rugged Solar CPV project

- 45 MW Tierra Del Sol CPV project

- 22 MW LanEast Solar CPV project

- 6.5 MW LanWest Solar CPV project

- 6.5 MW Desert Green Solar CPV project

OUTLOOK

In 2012, we expect that 81 MW of CSP and CPV projects will come on-line in the U.S., up from 12 MW in 2011. Much of the capacity expansion will come from the 30 MW CPV Alamosa Solar project. It should be noted that we have significantly reduced our concentrating solar forecast in light of the announcement that Blythe would be switched from trough to PV for economic reasons. The dramatic improvements in PV panel costs have put trough at a signifi cant cost disadvantage, and puts many of the planned trough projects at risk, as they may be difficult to finance or fail to receive regulatory approval. A massive wave of plant commissioning is expected in 2013, including Abengoa's Solana, BrightSource's Ivanpah 1, 2 and 3, and SolarReserve's Crescent Dunes. In later years, greater uncertainty regarding fi nancing, permitting and approvals surrounds the pipeline. The current pipeline of concentrating solar projects is over 9,000 MW, of which more than 5,000 MW have signed PPAs.

*References, data, charts or analysis from this Executive Summary should be attributed to the SEIA/GTM Research U.S. Solar Market Insight.

*All figures sourced are from GTM Research. For more detail on methodology and sources, visit www.gtmresearch.com/solarinsight.

GTM Research Solar Analysts:

Shayle Kann, Managing Director

Shyam Mehta, Senior Analyst

MJ Shiao, Solar Analyst

Andrew Krulewitz, Research Associate

Carolyn Campbell, Research Associate

Solar Energy Industries Association:

Tom Kimbis, Vice President, Strategy & External Affairs

Scott Fenn, Director of Research

Justin Baca, Senior Research Manager

Will Lent, Research & Policy Analyst

Shawn Rumery, Research Analyst

Mari Hernandez, Research Analyst