Solar Market Insight Report 2018 Q3

Other Links: Purchase the Full Report | Press Release

The quarterly SEIA/Wood Mackenzie Power & Renewables U.S. Solar Market InsightTM report shows the major trends in the U.S. solar industry. Learn more about the U.S. Solar Market Insight Report. Released September 13, 2018

Key Figures

- In Q2 2018, the U.S. market installed 2.3 GWdc of solar PV, a 9% year-over-year decrease and a 7% quarter-over-quarter decrease.

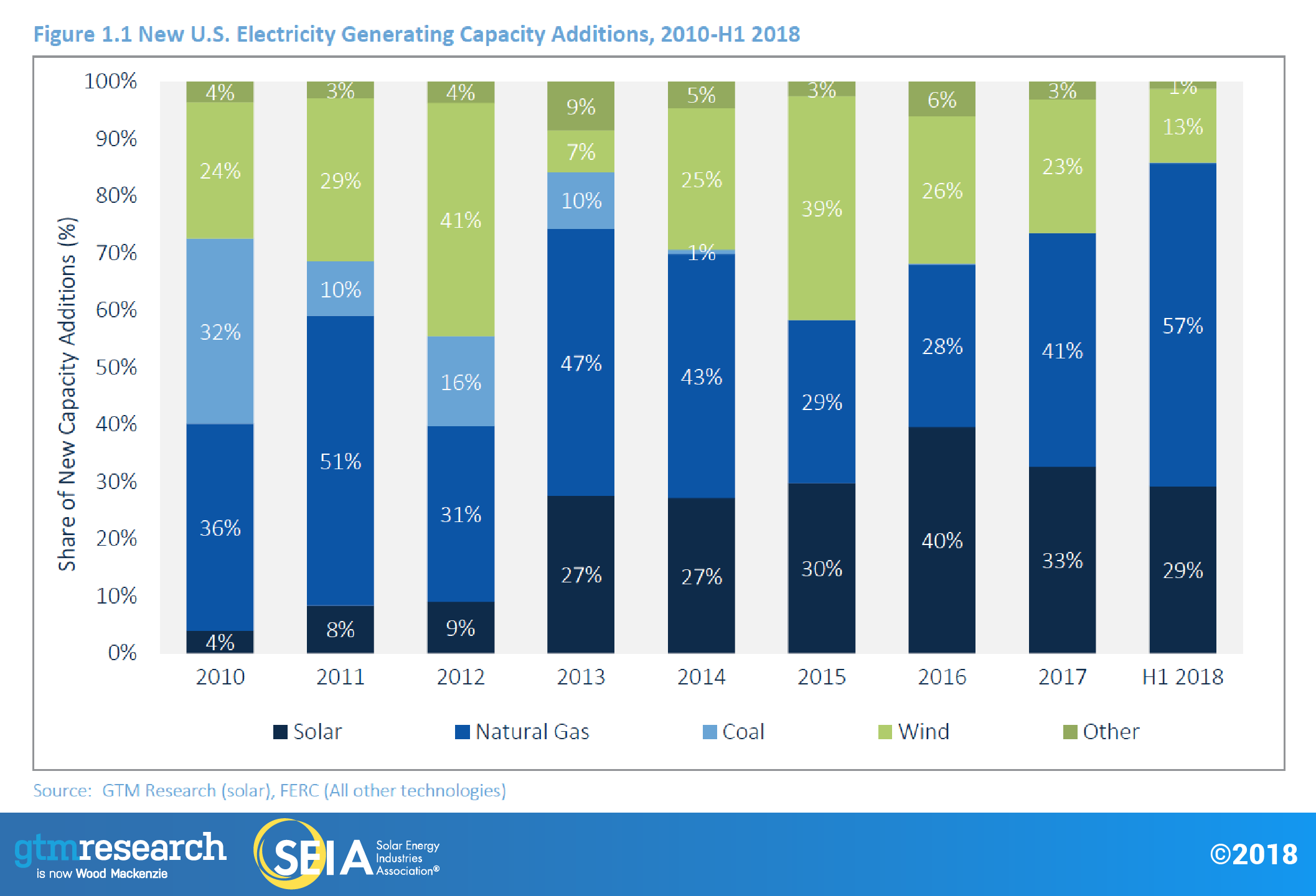

- In the first half of 2018, 29% of all new electricity generating capacity brought online in the U.S. came from solar PV.

- For a second consecutive quarter, the residential PV sector was essentially flat on both a year-over-year and quarter-over-quarter basis – an encouraging sign of market stabilization after a year in which the market contracted 15%.

- Non-residential PV fell 16% quarter-over-quarter and 8% year-over-year.

- Utility solar procurement experienced a massive rebound in the aftermath of Section 201 module tariff uncertainty. At 8.5 GWdc, the first half of 2018 stands as the largest half year of utility solar procurement ever.

- Corporate procurement of utility PV through physical PPAs, virtual PPAs and green tariffs has grown to account for 12% of projects in development.

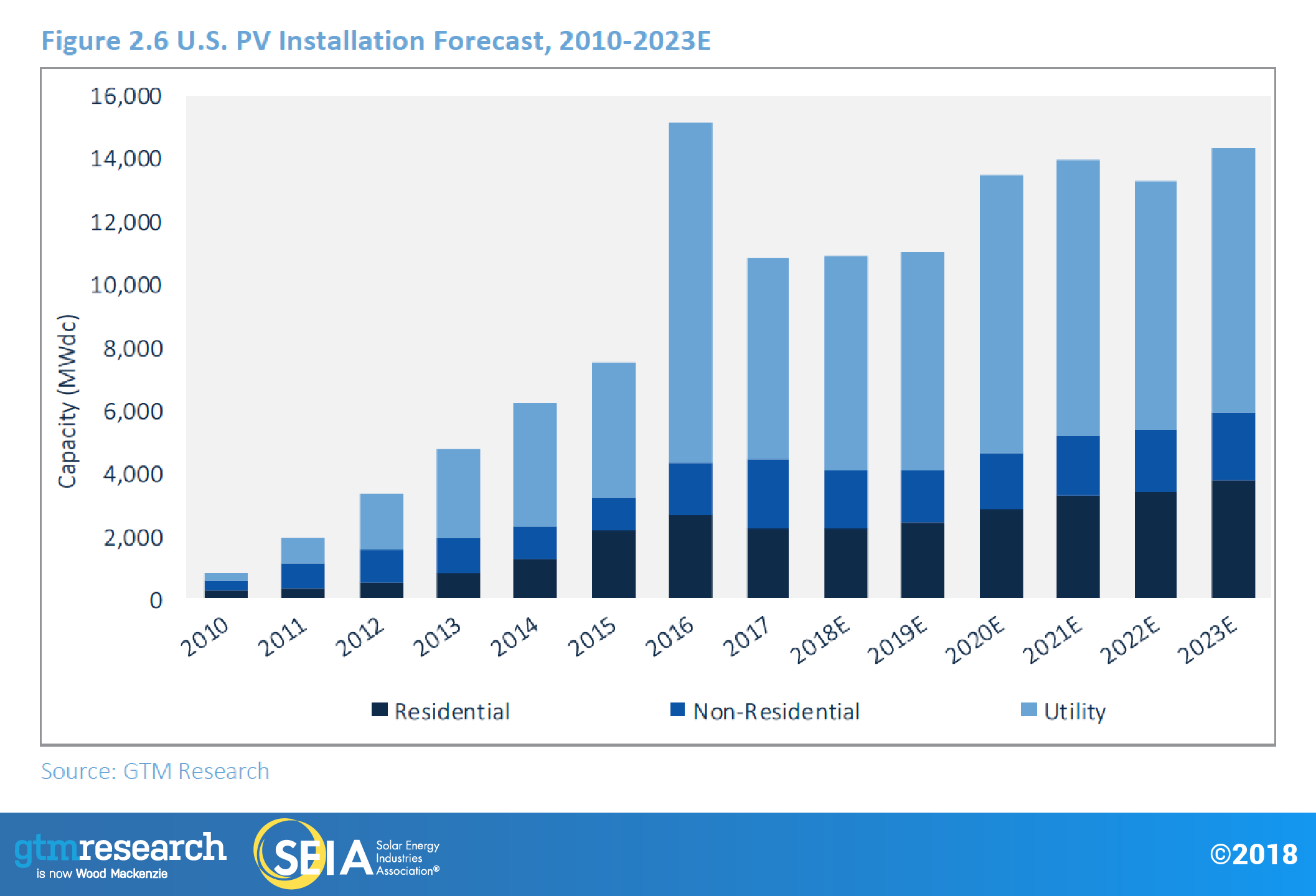

- GTM Research forecasts flat growth in 2018 vs. 2017, with another 10.9 GWdc of new PV installations expected.

- Total installed U.S. PV capacity is expected to more than double over the next five years. By 2023, over 14 GWdc of PV capacity will be installed annually

1. Introduction

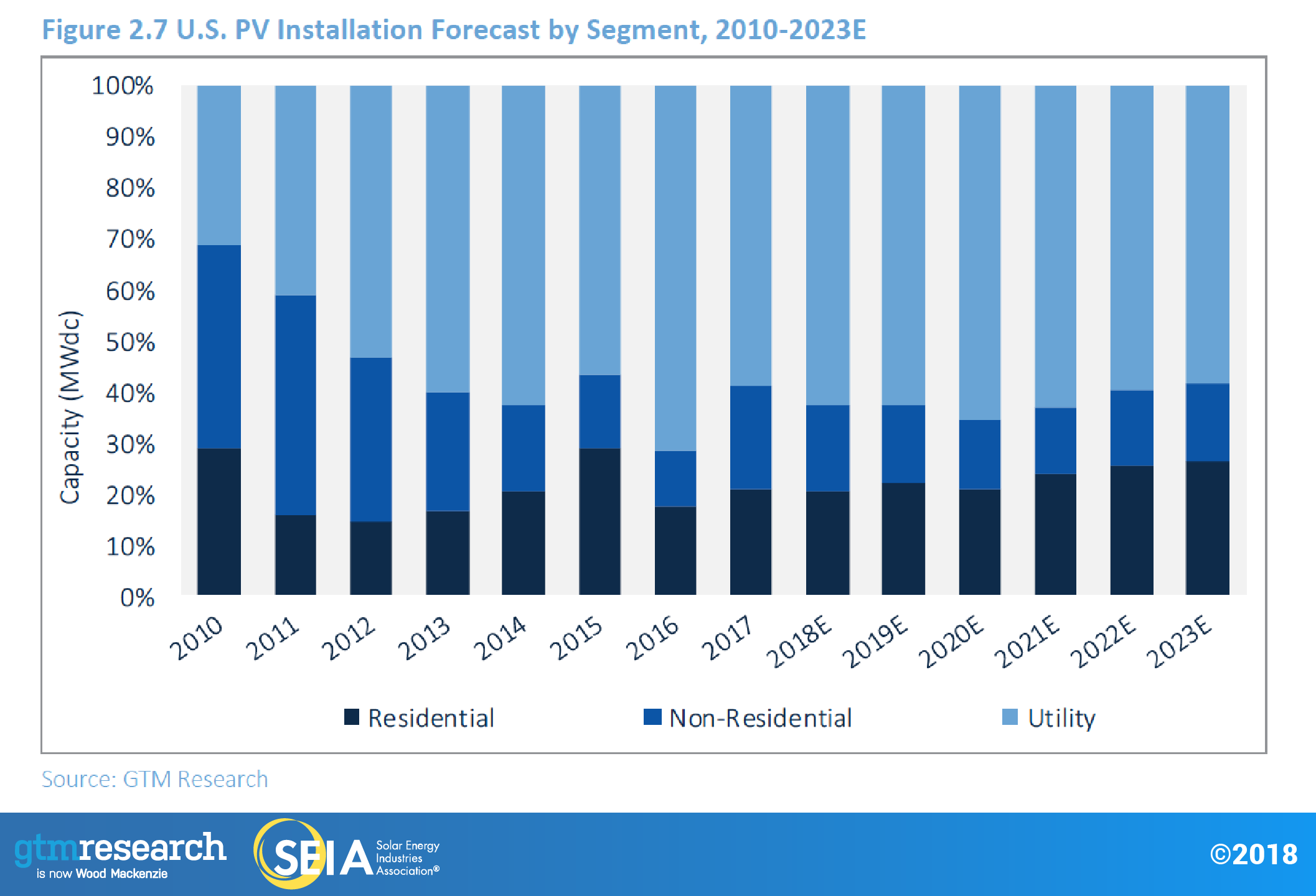

Over the first half of 2018, the U.S. solar market installed 4.7 gigawatts direct current (GWdc) of solar photovoltaic (PV) capacity. In line with historical trends, utility PV accounted for the bulk of PV installations at 55% of installed capacity through Q2 2018. Over the first half of the year, solar PV accounted for nearly 30% of new electricity generating capacity additions.

For residential PV, the story over the first half of 2018 relative to 2017 has been one of stabilization. After a year in which residential PV contracted 15%, the cadence of quarterly installation volumes has gradually increased since bottoming out in Q3 2017. The first half of 2018 has shown promising signs that the segment-wide customer-acquisition challenges that contributed to annual decline in 2017 have stabilized while also signaling the “bottoming out” for larger national installers that disproportionately contributed to volume contraction in 2017. However, customer acquisition issues have not disappeared. Of the top 10 markets in 2017, only three are expected to grow or remain flat in 2018. The decline in some major state markets will be offset by growth in emerging markets, and we accordingly expect a flat market in 2018.

Community solar continues to be a bright spot in non-residential PV. Primarily led by Minnesota and Massachusetts, well over 300 MW of community solar have been installed over the first half of 2018 and buildout will continue for the rest of the year in core and emerging state markets. That said, regulatory cliffs and policy reform have led to a decline in on-site C&I build-out in California and Massachusetts. In California, the pipeline of projects grandfathered in under solar-friendly time-of-use periods has begun to wane, and in Massachusetts, projects await the start of the SMART program.

The utility PV segment continues to make up the largest share of annual installations in the U.S. solar market. Q2 2018 was the 11th consecutive quarter with over 1.0 GWdc installed. 1.2 GWdc came online in Q2 2018, accounting for 55% of U.S. solar capacity installed. A total of 2.7 GWdc of projects are under construction and targeting completion in 2018.

Remarkably, procurement of U.S. utility solar has exploded over the first half of 2018 with a total of 8.5 GWdc of projects announced over that timeframe. This includes 26 projects that are 100 MWdc or larger – many of these projects were temporarily on hold during the first half of 2017 due to uncertainty surrounding the Section 201 module tariffs. Once lower-than-expected module tariffs were announced in January 2018, developers and utilities began announcing new projects. However, not every project fared the same. Some previously announced projects were canceled or delayed due to the tariffs. As we move toward 2019, we expect to see continued procurement growth as developers look to secure projects they can bring online before the federal Investment Tax Credit (ITC) steps down to 10% in 2022.

Federal Policy Update: IRS Issues Guidance on Commence Construction for ITC Qualification

Q2 2018 also saw some positive developments on federal policy. In June, the IRS issued Notice 2018-59, which provides guidance on commence-construction rules for projects qualifying for the Section 48 credit of the ITC. This guidance allows a project to claim a higher ITC rate based on the year it commences construction, with two methods available to claim that higher tax credit.

- One approach is called the physical work test, which a requires a project to begin physical work of a significant nature. Satisfying this requirement can include offsite work, such as manufacturing of hardware, and onsite installation work. This is generally viewed as a more challenging method to qualify for commence construction, as evidenced by the wind industry, which has largely refrained from using this method.

- It is expected that the more common method to qualify for commence construction will be the 5 percent safe harbor rule, which requires a project to incur 5% or more of total system costs.

Looking ahead, this IRS guidance means that if a project deploys 5% of capital costs in 2019, it can roll the 30% ITC into subsequent years, so long as the project is completed by the end of 2023. While the IRS guidance on commence construction doesn’t come as a huge surprise, it offers a fairly favorable interpretation of the statute and provides certainty on tax policy that was previously unconfirmed.

1.1. Section 201 and Module Tariff Update

In June 2018 the IRS released guidance for the requirements for commence construction of solar energy projects and qualifying for the solar Investment Tax Credit. This guidance disproportionately impacts the utility solar segment given its longer project timelines. Developers would anchor projects in a given year by paying 5% of the total facility cost (safe harbor) or starting work in a significant nature and continuously building (continuous construction). As expected, the ITC steps down from 30% for all projects anchored in 2019 to 26% for all projects anchored in 2020, 22% for all projects in 2021, and 10% for all projects anchored in 2022 or after. All projects claiming the ITC at 22% or higher must complete construction by December 31, 2023. While this guidance would tend to pull project demand into 2020, demand pull-in effects are muted by several factors:>

- Module tariffs: Ad valorem tariffs on modules stand at 30% in 2018 and decline by 5 percentage points annually to 15% in year 4. This will drive developers to anchor projects in 2019 but procure modules in 2020 or later, thereby driving target commercial operation dates (COD) further out.

- Module price decline/China oversupply: While GTM has always expected PV module prices to drop on a year-over-year basis, the decline has been faster than anticipated. In June 2018, China announced installation caps and a reduction to the country’s feed-in tariff, which will result in significantly reduced demand from China and an oversupply of solar modules in the global market. These two factors together could incentivize developers to delay module procurement and could lead them to conclude it is more advantageous to forgo the 30% ITC for 26% or 22% to secure lower-cost solar panels.

- Technology risk: Anchoring projects early also carries some technology risk. Not only are modules declining in cost, they are increasing in efficiency. Securing a module contract too early could mean a developer is locked into using low-efficiency modules that they paid too much for. Anchoring a project by purchasing trackers or inverters could lock projects into tracker designs that are unwanted or inverters that are less efficient or more expensive than newer models.

Many developers could determine that the long-term risk of anchoring utility-scale projects more than 12 months before their COD outweighs the risks of accepting a 26% or 22% ITC. A small number of developers will anchor projects in 2019 for 2021 or later, but this is likely to occur in only a handful of instances such as continuous construction of several projects on the same site, bringing on a project early with a 1- or 2-year bridge PPA, or selling merchant power before its PPA begins. The year 2022 will become the year most susceptible to demand pull-in as the ITC drops from 22% to 10% and developers complete projects early.

2. Photovoltaics

2.1. Market Segment Trends

2.1.1. Residential PV

Key Figures

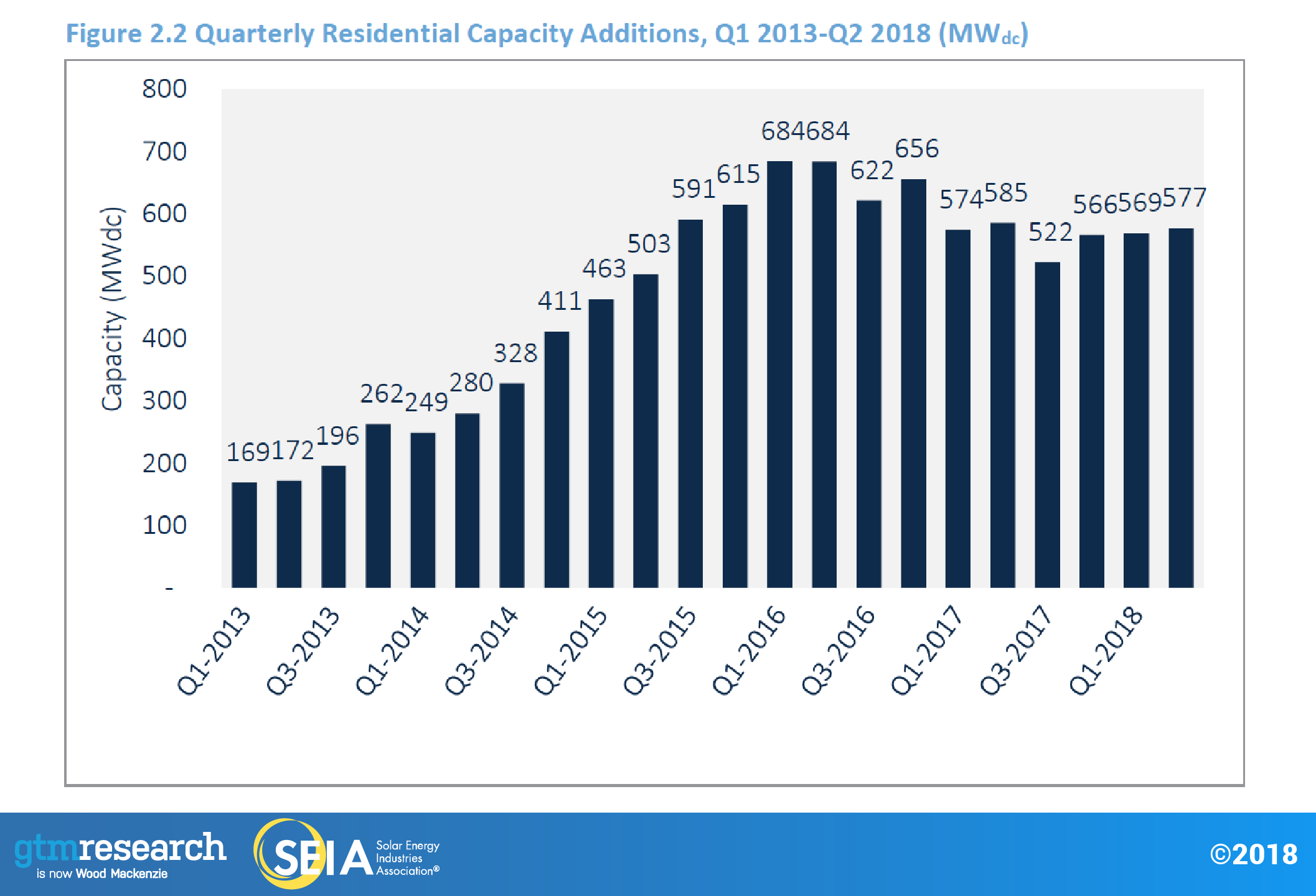

- 577 MWdc installed in Q2 2018

- Flat quarter-over-quarter and year-over-year

After a year in which the residential market saw 15% contraction, installation numbers over the first half of 2018 show promising signs that segment-wide customer-acquisition challenges may be abating in 2018 as volume contraction appears to be leveling out across the national installer landscape.

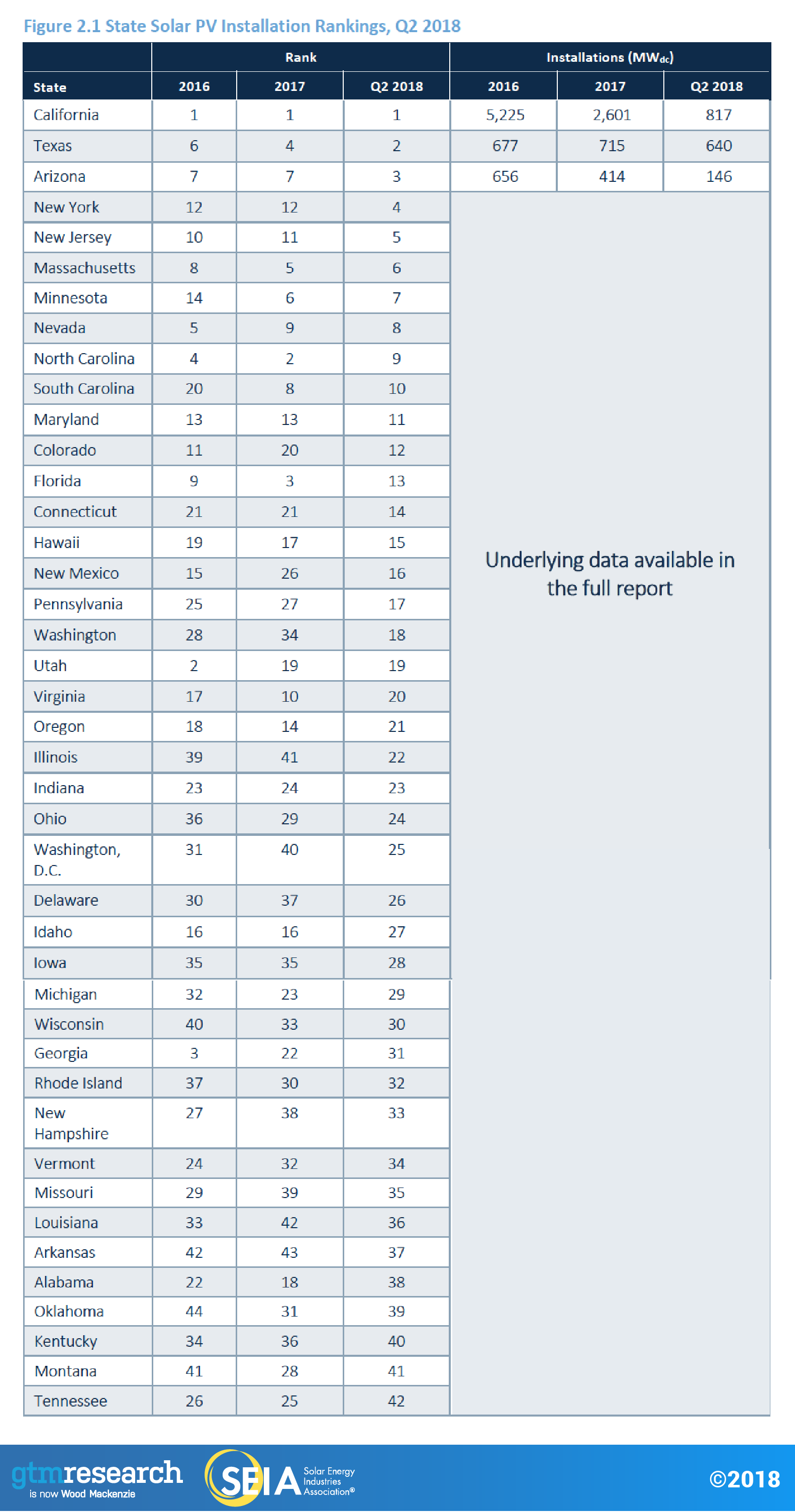

However, major markets continue to exhibit signs of weakness – six of the top 10 state markets fell year-over-year in Q2 as the lingering effects of national installer pullback and customer acquisition issues continue to constrain growth. But despite major market weakness, a handful of emerging markets are offsetting the decline. Nevada, for instance, showed the highest quarter-over-quarter installation growth in megawatt terms out of all states as installers begin to see installations climb after re-establishing sales operations once net metering was reinstated. Similarly, Florida’s residential market continues to grow as more third-party ownership (TPO) providers seek PSC permission to sell leases in the state. That said, emerging market growth has only been able to offset major market decline. Accordingly, we expect a flat 2018.

2.1.2. Non-residential PV

Key Figures

- 453 MWdc installed in Q2 2018

- Down 16% from Q1 2018

- Down 8% from Q2 2017

While 2017 was the primary beneficiary of regulatory demand pull-in in California and major Northeast markets, the first half of 2018 has also seen some spillover of this pipeline. California witnessed record non-residential installations in 2017 from developers rushing to install projects to meet a (since-lifted) deadline to be grandfathered in under more favorable, solar-friendly time-of-use rates. This pipeline continues to be built out into 2018, although it is expected to wane over the second half of 2018. Meanwhile, the build-out of Xcel Energy’s robust community solar pipeline in Minnesota continues to account for a significant share of non-residential growth, with over 150 MWdc built out over the first half of the year.

2.1.3. Utility PV

Key Figures

- 1,243 MWdc installed in Q2 2018

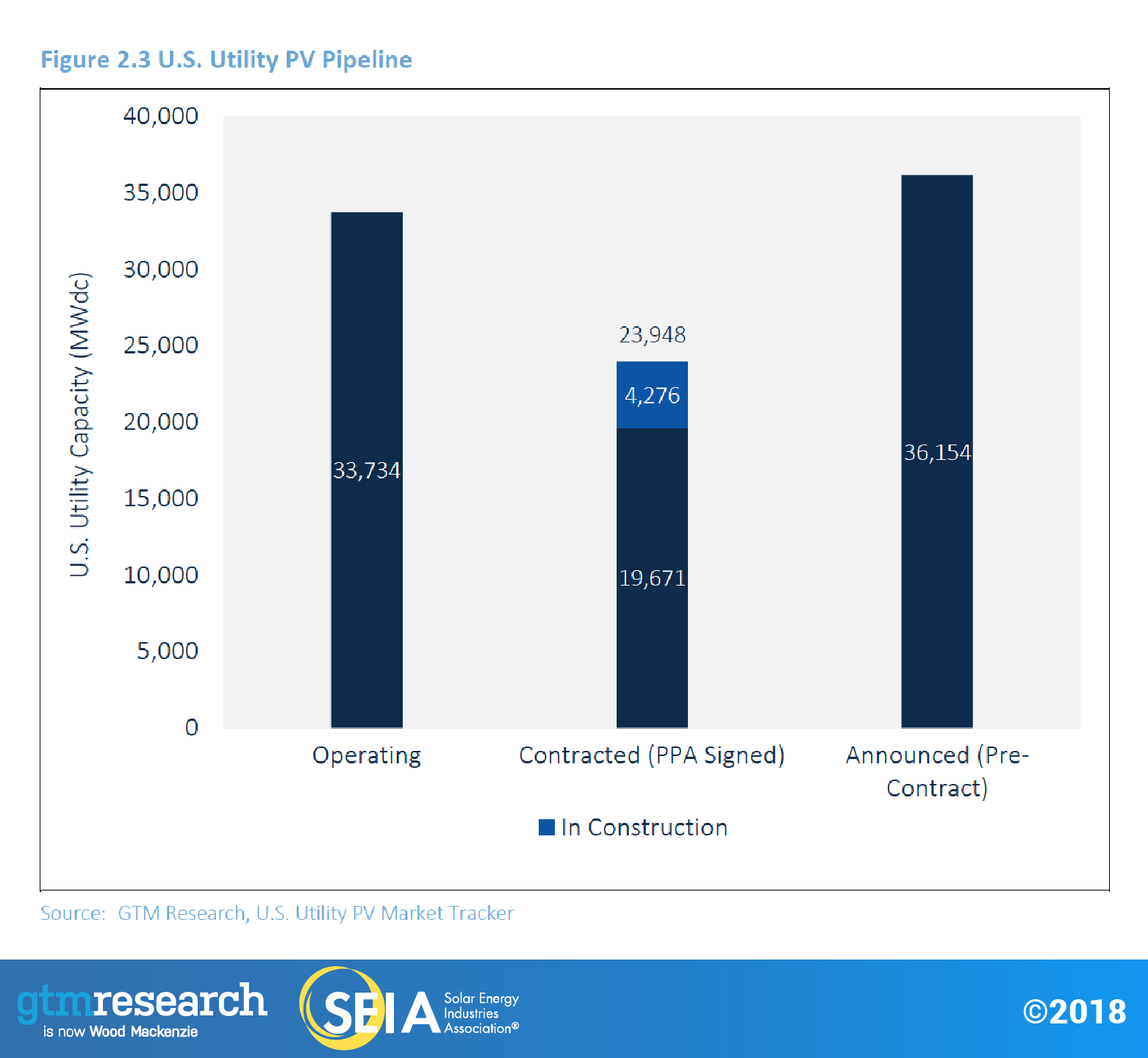

- Contracted utility PV pipeline currently totals 23.9 GWdc

- 11th consecutive quarter in which utility PV added over 1 GWdc

Utility PV continues to make up the largest share of annual installed capacity in the U.S. solar market. The second quarter of 2018 was the 11th consecutive quarter with over 1.0 GWdc installed. 1.2 GWdc came online in Q2 2018, accounting for 55% of U.S. capacity installed. A total of 2.7 GWdc of projects are under construction and targeting 2018 completion.

Remarkably, procurement of U.S. utility solar has exploded over the last two quarters with a total of 8.5 GWdc of projects announced in the first half of 2018 including 26 projects 100 MWdc or larger. While the decline in module and system component costs relative to previous expectations is a factor, the uptick in procurement can be attributed to projects that were temporarily on hold in early 2017 while developers waited for clarity on section 201 tariffs. Once module tariffs were announced in January 2018 and uncertainty was removed, developers and utilities began announcing new projects.

The surge in procurement has caused GTM’s forecast over the outlook period (2018-2023) to grow by 1.9 GWdc over the last quarter. Though the market continues to recover, GTM’s utility PV forecast for 2018-2023 is still 7.9% lower than before Section 201 tariffs were announced. Many developers have reported that for a small portion of their pipeline, they are either still renegotiating PPAs or have had to cancel projects entirely due to the addition of module tariffs. As we move toward 2019, we expect to see procurement to continue growing as developers look to secure projects they can bring online before the ITC steps down to 10% in 2022.

Near term, our 2018 forecast has grown from 6.6 GWdc to 6.8 GWdc as our confidence in projects’ ability to come online increases. 2019 continues to be the year most heavily impacted by tariffs with new procurement primarily targeting 2020 or later. GTM believes this is both a result of projects originally slated for 2019 pushing out target COD dates and developers looking to anchor projects to a 30% ITC in 2019 while procuring modules at a lower tariff rate in 2020.

Medium term, 2020 and 2021 have seen a cumulative 1.4 GWdc increase due to the uptick in procurement from utilities like Wisconsin Public Service Corporation, NV Energy, Florida Municipal Power Agency, and Dominion that have all announced hundreds of megawatts’ worth of new development. Most RFPs released target 2020 or 2021 CODs, which will continue to drive growth in these years. Due to the ITC stepping down and the fear that interest rates may rise, several corporations have suggested that 2020 and 2021 may be the optimal time to sign a large offtake agreement.

The bulk of 2022 capacity additions will come from developers leveraging the 22% ITC before it steps down to 10%. 2023 will be the first year where over half of utility solar projects brought online will leverage a 10% ITC. Despite the ITC drop-off, we expect the solar market to continue growing. Levelized cost of energy (LCOE) analysis of generation resources by GTM Research and Wood Mackenzie shows that by 2023, the LCOE of 20 MW of utility PV will be less than that of onshore wind in 49 state markets. This will result in more utilities turning to solar over wind for renewables generation and driving continued growth through the 2023 timeframe.

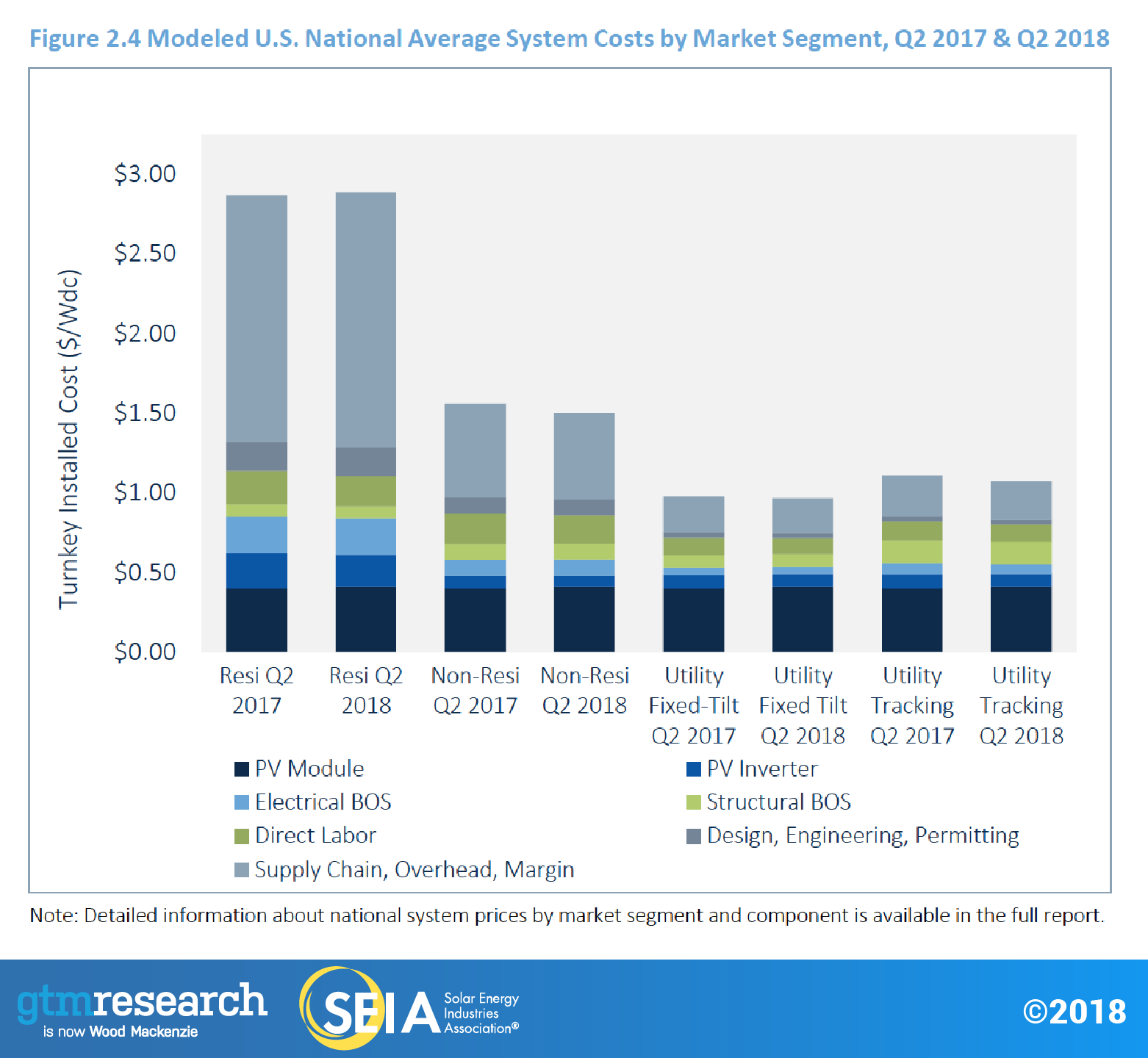

2.2. National Solar PV System Pricing

We employ a bottom-up modeling methodology to track and report national average PV system pricing for the major market segments. This methodology is based on tracked wholesale pricing of major solar components and data collected from interviews with major installers.

In Q2 2018, system pricing fell in all market segments. System pricing fell by 1.7%, 3.2%, 4.9% and 5.7% in the residential, non-residential, utility fixed-tilt and utility single-axis tracking markets, respectively. In Q1 2018, average system prices finally started to fall after two quarters of rising module prices. This was due almost entirely to the anticipated impact of the Section 201 module tariffs. After the tariff’s implementation, demand slowed and both pre-tariff module and system prices fell. In Q2 2018 module pricing fell sharply as the global module market braced for oversupply, predominantly due to lower demand from the Chinese market. As a result, in every market segment besides residential PV, system pricing is at its lowest level ever. Even in residential PV, where customer acquisition costs have risen in the past year, system prices are only two cents above their Q2 2017 historic low of $2.87/Wdc. On the balance-of-systems side, even with new tariffs impacting some players, the pre-201 norms are back in place, with hyper-aggressive pricing to shore up market share.

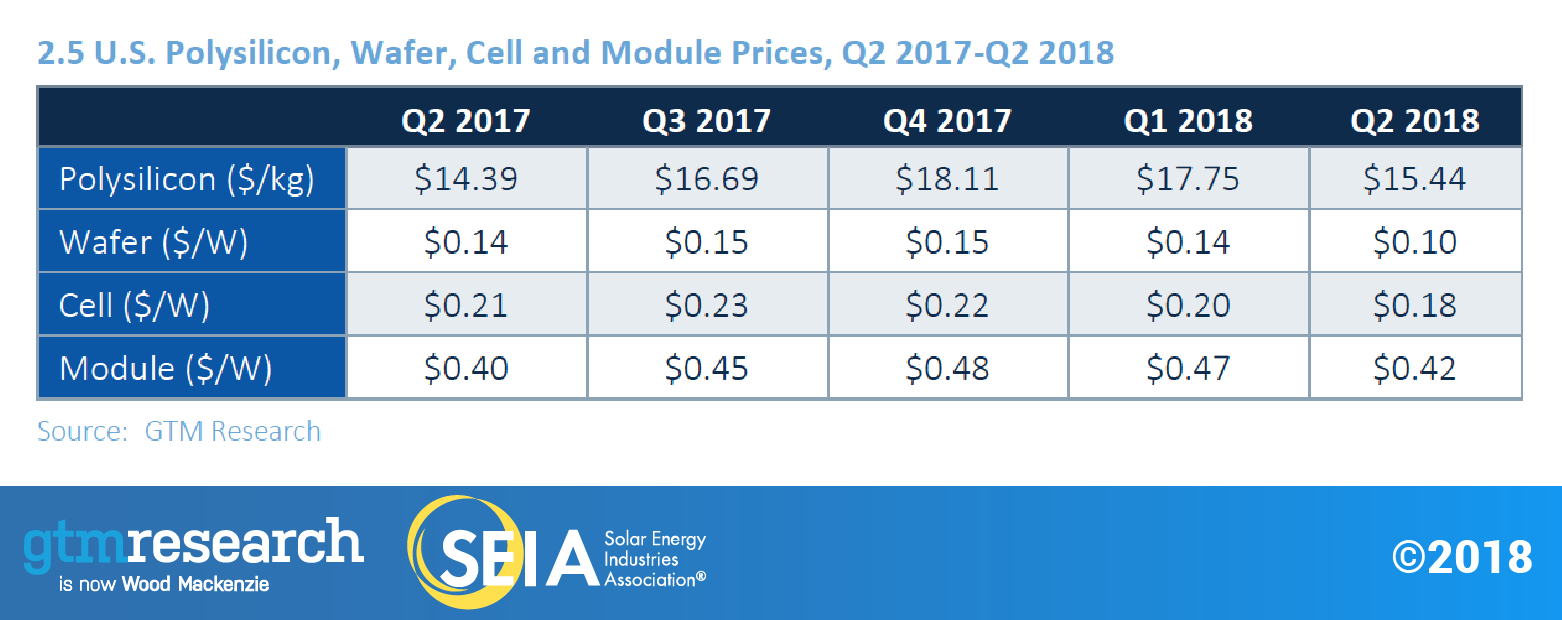

2.3. Component Pricing

Component pricing fell in Q2 2018, with global demand weakening and buyers pressuring suppliers to reduce prices in every part of the value chain.

- For polysilicon, the quarterly average price fell 13% quarter-over-quarter to $15.44/kg in Q2 2018. Polysilicon prices fell as downstream demand declined, as well as in response to buyer pressure. With wafer and cell margins tight, buyers demanded polysilicon suppliers reduce high prices.

- Multi wafer and cell price decline was more aggressive, with quarterly average prices hitting a respective $0.10/W to $0.18/W. Price trends were driven by low demand and high inventory levels.

- Module prices fell significantly due to weak demand and increasingly competitive bidding as suppliers tried to lock in buyers, with multi module prices averaging $0.42/W in Q2 2018. The mono PERC module premium over standard multi decreased from ~ 5-6 cents/W to ~3-4 cents/W.

2.4. Market Outlook

GTM Research forecasts a flat U.S. solar market in 2018. Utility PV is expected to grow 7% as most projects targeting 2018 completion were able to secure tariff-free module supply. Meanwhile, the non-residential market is forecasted to see an annual decline. The pipeline of projects grandfathered in under a more favorable policy and incentive environment is waning despite a record-breaking year for community solar expected in 2018. Though most major residential markets are expected to contract again in 2018, emerging market growth in states like Florida and Nevada will help to offset major market weakness, ultimately resulting in a flat 2018 for that market segment.

For utility PV, 2019 continues to be the year most heavily impacted by tariffs. GTM believes this is both a result of projects originally slated for 2019 pushing out target COD dates and developers looking to anchor projects to a 30% ITC in 2019 but procure modules at a lower tariff rate in 2020. Medium term, 2020 and 2021 have seen a cumulative 1.4 GWdc increase due to the uptick in procurement from utilities that have all announced hundreds of megawatts of new development after tariffs were finalized in January. The bulk of 2022 capacity additions will come from developers leveraging the 22% ITC before it steps down to 10%. However, 2023 is still expected to see a rebound in growth as the module tariffs phase out.

For residential PV, a flat 2018 allows for a more robust rebound in 2019 as the market aligns to the growth expectations of small and medium-sized installers leveraging less expensive customer-acquisition channels. National growth rates will hit 10% in 2020 as emerging states scale and growth rates hit the mid-teens beginning in 2020, in part bolstered by the California mandate for all new residential housing to include rooftop solar in addition to the new Illinois Adjustable Block Incentive program, which will begin to bear fruit in the new decade. Together with Florida, these three states will account for 60% of residential capacity additions between 2018-2023.

Meanwhile, the non-residential PV market is expected to experience two consecutive down years as the grandfathered-project pipeline wanes in 2018 and the market acclimates to a reduced incentive environment across major state markets in 2019. However, this will be incrementally offset starting in 2020 as the next wave of states with robust community solar mandates – New York, Maryland, Illinois – begin to see the realization of those pipelines. Increasing solar-plus-storage viability will also begin to have an impact on non-residential demand. By 2023, we expect that roughly 30% of non-residential PV will be supported by community solar, and another 20% or so will come from solar-plus-storage projects.

By 2020, 28 states in the U.S. are expected to be 100+ MWdc annual solar markets, with 25 of those states being home to more than 1 GWdc of operating solar PV. This compares to only two states with 100+ MWdc annual solar markets in 2010.

Forecast details by state (45 states plus Washington, D.C.) and market segment through 2023 are available in the full report.

About the Report

U.S. Solar Market Insight® is a quarterly publication of Wood Mackenzie, Limited (formerly known as GTM Research) and the Solar Energy Industries Association (SEIA)®. Each quarter, we collect granular data on the U.S. solar market from nearly 200 utilities, state agencies, installers and manufacturers. This data provides the backbone of this U.S. Solar Market Insight® report, in which we identify and analyze trends in U.S. solar demand, manufacturing and pricing by state and market segment. We also use this analysis to look forward and forecast demand over the next five years. All forecasts are from Wood Mackenzie, Limited; SEIA does not predict future pricing, bid terms, costs, deployment or supply.

- References, data, charts and analysis from this executive summary should be attributed to “Wood Mackenzie, Limited/SEIA U.S. Solar Market Insight®."

- Media inquiries should be directed to Wood Mackenzie’s PR team ([email protected]) and Morgan Lyons ([email protected]) at SEIA.

- All figures are sourced from Wood Mackenzie, Limited. For more detail on methodology and sources, visit www.gtmresearch.com/solarinsight.

- Wood Mackenzie Power and Renewables (WM P&R) partners with Clean Power Research to acquire project-level datasets from participating utilities that utilize the PowerClerk product platform. For more information on Clean Power Research’s product offerings, visit https://www.cleanpower.com/.

Our coverage in the U.S. Solar Market Insight reports includes 43 individual states and Washington, D.C. However, the national totals reported include all 50 states, Washington, D.C. and Puerto Rico.

Detailed data and forecasts for 43 states and Washington, D.C. are contained within the full version of this report, available at www.greentechmedia.com/research/ussmi.

Author's Note: Revision to the U.S. Solar Market Insight report title

WM P&R and SEIA have changed the naming convention for the U.S. Solar Market Insight report series. Starting with the report released in June 2016 onward, the report title will reference the quarter in which the report is released, as opposed to the most recent quarter in which installation figures are tracked. The exception will be our Year in Review publication, which covers the preceding year’s installation volumes despite being released during the first quarter of the current year.

About the Authors

GTM Research | U.S. Research Team

Austin Perea, Senior Solar Analyst (lead author)

Cory Honeyman, Associate Director of U.S. Solar

Colin Smith, Senior Solar Analyst

Allison Mond, Senior Solar Analyst

MJ Shiao, Global Lead, Renewables and Emerging Technologies

Jade Jones, Senior Solar Analyst

Scott Moskowitz, Senior Solar Analyst

Benjamin Gallagher, Senior Solar Analyst

Michelle Davis, Senior Solar Analyst

Solar Energy Industries Association | SEIA

Shawn Rumery, Director of Research

Aaron Holm, Data Engineer

Rachel Goldstein, Research Analyst

Justin Baca, Vice President of Markets & Research