Solar ITC Impact Analysis

Click here to download a PDF of this factsheet. This analysis was conducted prior to the passage of a long-term extension of the ITC that differed from the assumptions based on these findings. To find out more about the impacts of the extension that was ultimately passed, click here.

Data supporting this analysis can be purchased! Learn more.

How an Extension of the Solar Investment Tax Credit Would Affect the Industry

Background

The Investment Tax Credit (ITC) is the solar industry’s most important public policy. As such, SEIA commissioned an independent analysis from Bloomberg New Energy Finance (BNEF) to analyze the impact of the ITC on the industry – and what the U.S. stands to lose if Congress lets this policy expire in 2016.

Methodology

The BNEF analysis is based on two scenarios:

- Current policy as written – the residential credit (under section 25D) is eliminated and the commercial credit (section 48) is reduced from 30% to 10%

- A five-year extension of the ITC at 30% for both residential and commercial use, with a commence construction clause added. Under this scenario, the ITC extension is confirmed mid-2016

{kind=link}

{kind=link}

{kind=link}

Key Takeaways

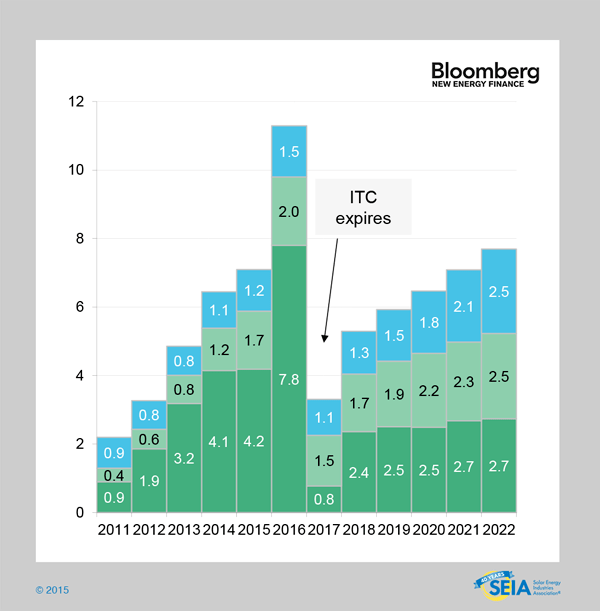

If the ITC expires at the end of 2016, installed solar capacity is expected to fall by nearly 8 gigawatts (GW) from 2016-2017. Solar project levels would plummet from 11.2 GW in 2016 to 3.2 GW in 2017 – the lowest annual level since 2012.

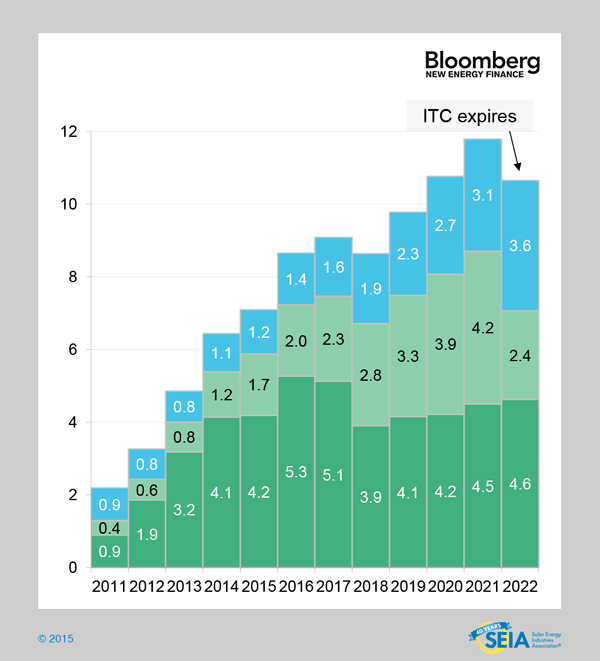

However, if the ITC is extended, more than 69 GW of new solar power would be built across America between 2016 and 2022, representing a 22 GW increase over current policy.

Growth under an ITC extension cuts across all segments. The utility-scale segment can expect to install more than 31 GW between 2016-2022, 10 GW more than the no-ITC scenario. The commercial segment is expected to install an additional 5 GW with an ITC extension, while the residential segment will install an additional 7 GW.

What an ITC Extension Means

If the ITC is extended, by 2022 more than 95 GW of solar power will be installed in the U.S., generating nearly 144 Terawatt-hours (TWh) of electricity each year. This means that:

- The solar industry would generate enough electricity to power 19 million homes

- Solar would account for 3.5% of U.S. electricity generation – up from just 0.1% in 2010

- Every year, solar power would offset 100 million metric tons of carbon dioxide (CO2) emissions, equivalent to shuttering 26 coal-fired power plants or taking 20 million cars off the roads

The “ITC cliff” in 2017 under current policy is far steeper than the drop following the end of an extension in 2022. The 2016-17 drop represents a 71% decline in solar deployment, but under an extension scenario, due to lower prices, commence construction language and industry maturity, the drop is only 10% from 2021-22.

Economic Impact

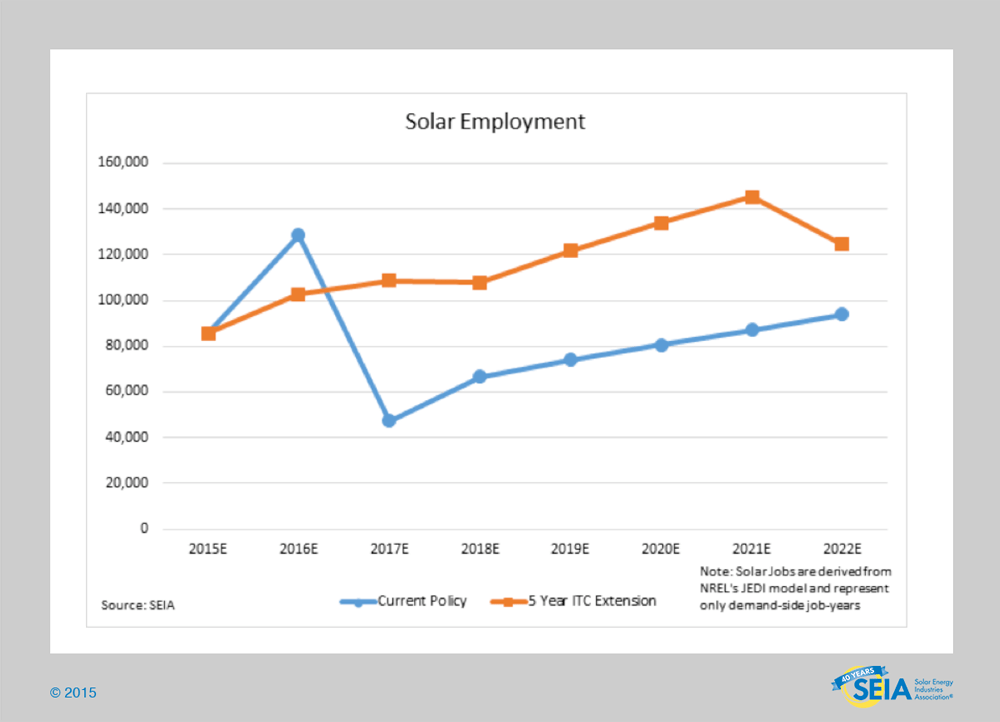

Using the National Renewable Energy Laboratory’s (NREL) Jobs and Economic Development Impacts model (JEDI), SEIA analyzed BNEF data that covers the ITC’s impact on jobs and economic investment.

Without an ITC extension, the U.S. stands to lose 80,000 solar jobs[1] in 2017, plus an additional 20,000 jobs in related affected industries, for a total loss of 100,000 American jobs. In contrast, an ITC extension would yield 61,000 more solar jobs in 2017 than a no-ITC extension scenario, and 58,000 more jobs in 2021. Between 2016 and 2022, solar industry employment is 32% higher with an ITC extension than without.

Total investment in the U.S. economy from solar during 2016-22 is projected to be more than $124 billion, $39 billion more than if the ITC expires.

[1] Solar jobs are derived from NREL's JEDI model and represent demand-side job-years. They are not comparable to the Solar Foundation’s job census which counts both demand and supply-side jobs and uses a different methodology. For more information see http://www.nrel.gov/analysis/jedi/ and http://www.thesolarfoundation.org/solar-jobs-census/.”

Click here to download a Powerpoint presentation summarizing the analysis from BNEF