Solar Market Insight 2015 Q4

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Purchase the Full Report | Press Release

The quarterly SEIA/GTM Research U.S. Solar Market Insight™ report shows the major trends in the U.S. solar industry. Learn more about the U.S. Solar Market Insight Report.

Key Figures

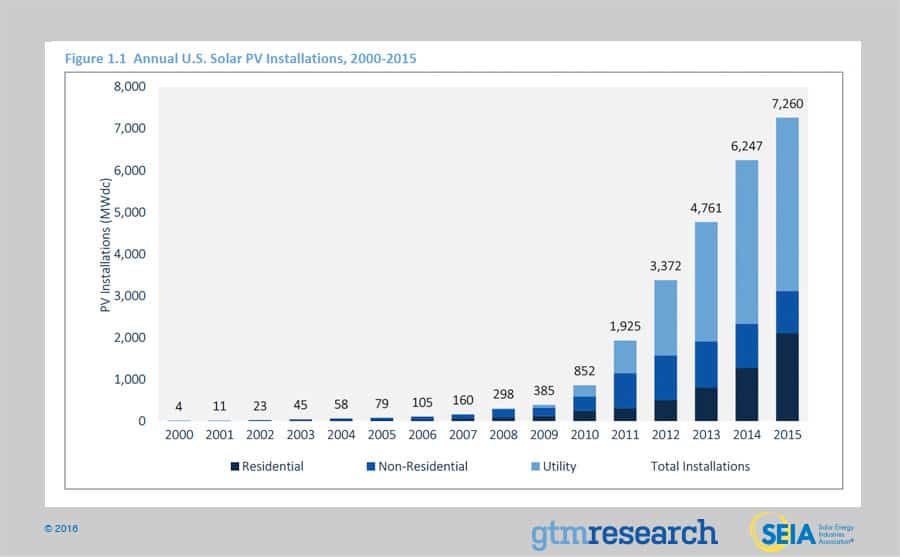

- The U.S. installed 7,260 MWdc of solar PV in 2015, the largest annual total ever and 16% above 2014.

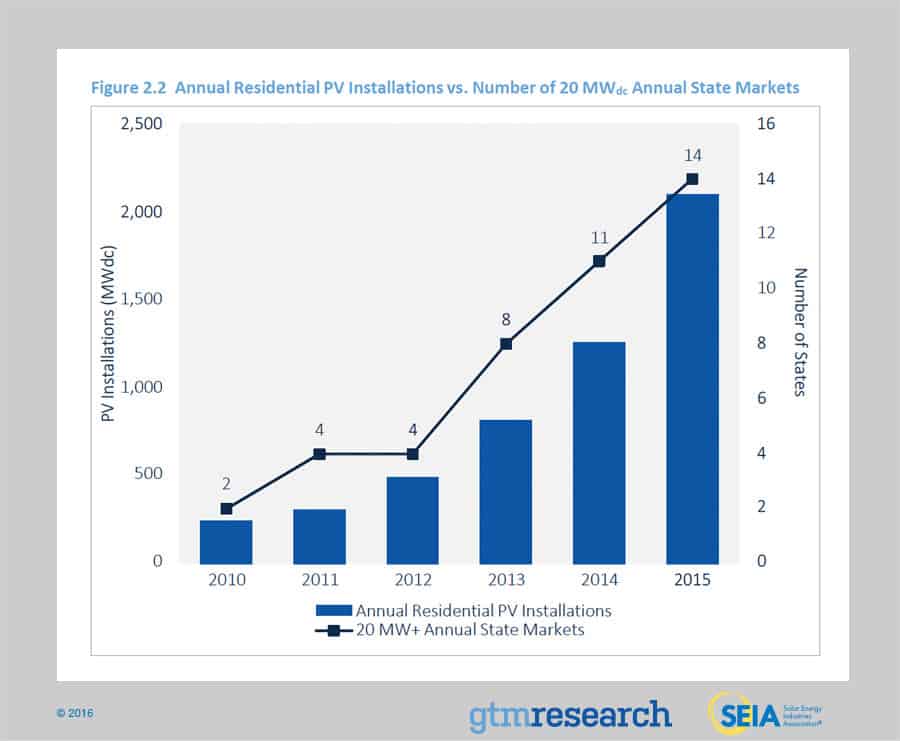

- Residential PV was once again the fastest-growing sector in U.S. solar, installing over 2 GWdc for the first time and growing 66% over 2014.

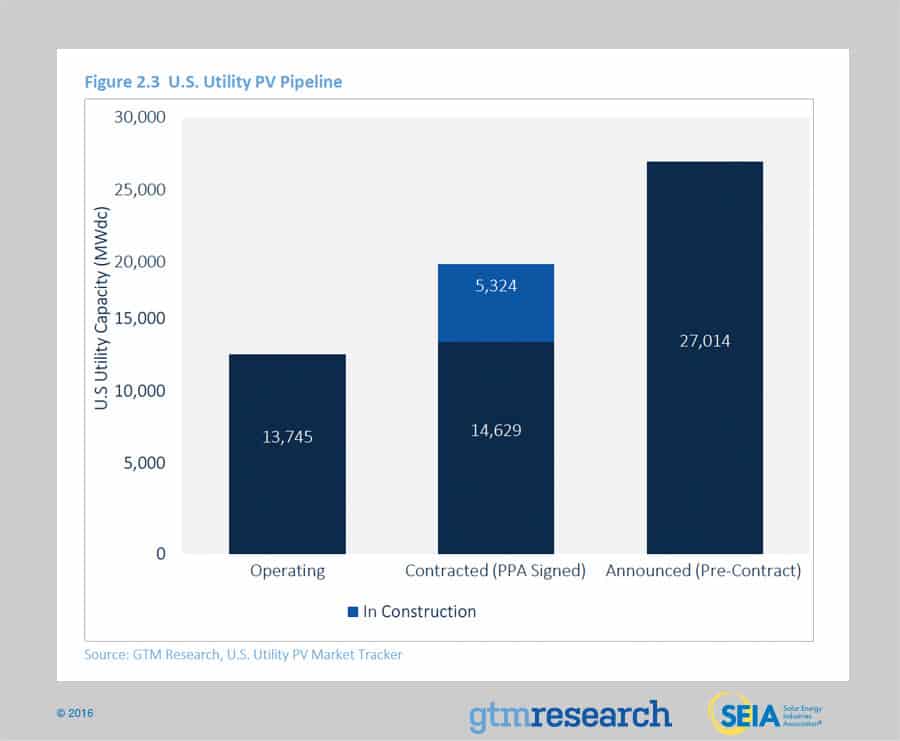

- Utility PV also had a record year with over 4 GWdc installed, up 6% over 2014, with nearly 20 GWdc still in development.

- Thirteen states installed over 100 MWdc of solar each in 2015, up from nine in 2014.

- 110 MW ac of concentrating solar power (CSP) capacity came on-line in late 2015, when SolarReserve’s Crescent Dunes project began sending electricity to the grid.

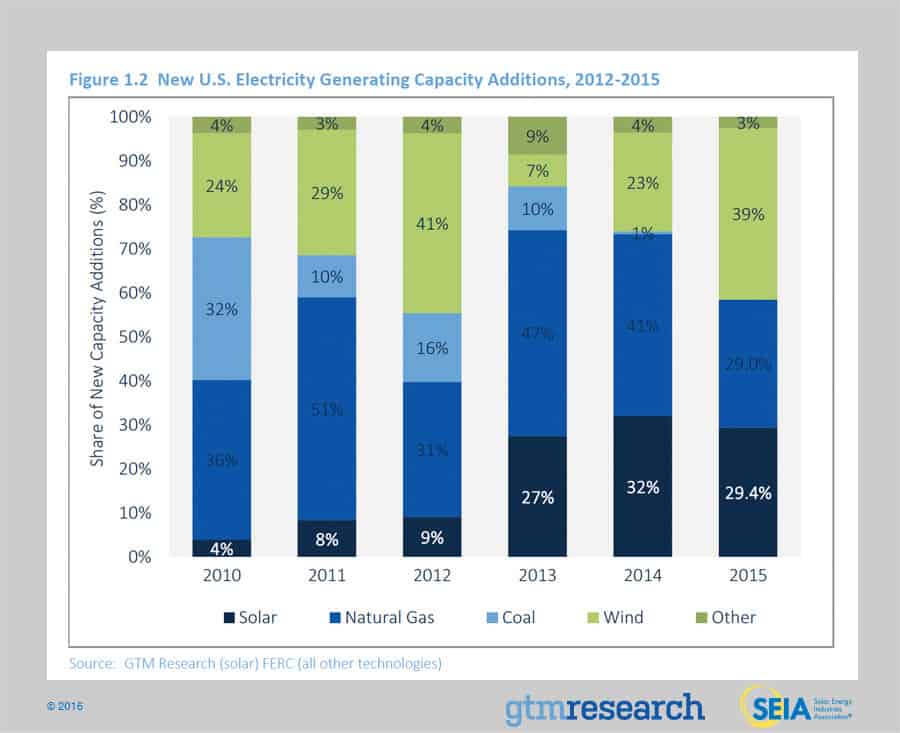

- For the first time ever, solar beat out natural gas capacity additions, with solar supplying 29.4% of all new electric generating capacity brought on-line in the U.S. in 2015.

- Cumulative solar PV installations surpassed 25 GWdc by the end of the year, up from just 2 GWdc at the end of 2010. Cumulative CSP capacity now stands at 1.8 GWac.

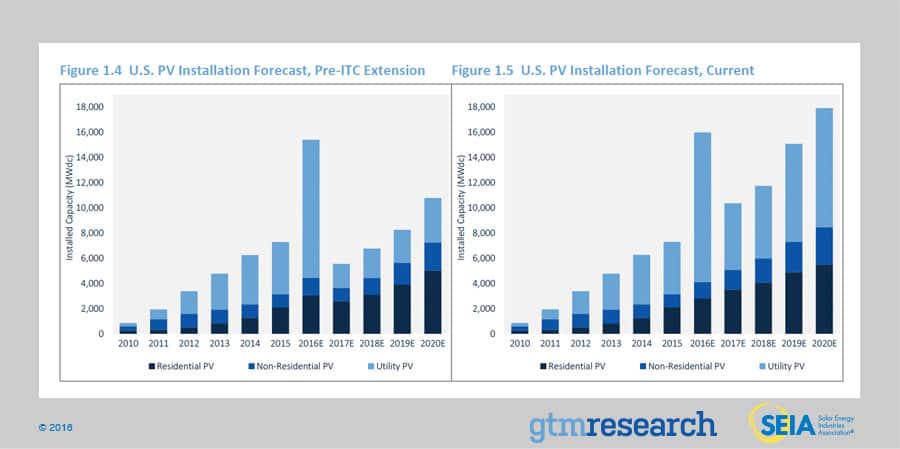

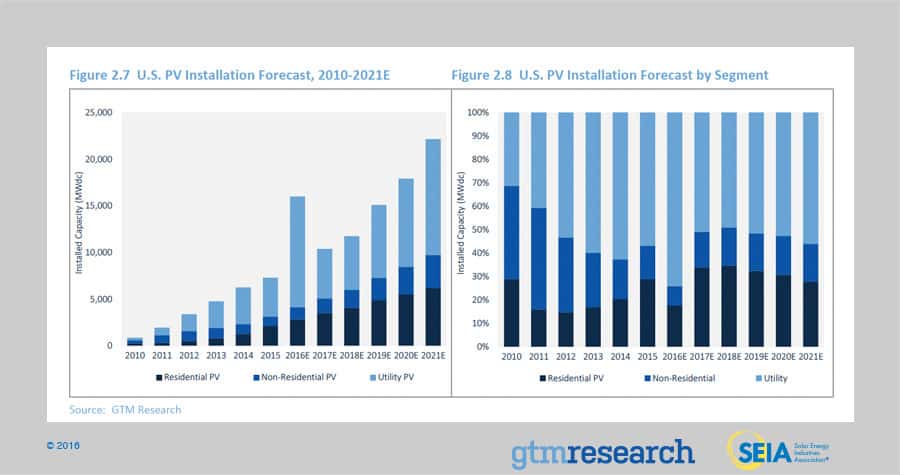

- GTM Research forecasts that 16 GWdc of new PV installations will come on-line in 2016, up 120% over 2015. Utility PV is expected to drive the majority of demand, accounting for nearly three-fourths of new installations.

1. Introduction

2015 was a momentous year for solar power in the United States. Solar PV deployments reached an all-time high of 7,260 megawatts direct current (MWdc), up 16% over 2014 and 8.5 times the amount installed five years earlier. Total operating solar PV capacity reached 25.6 GWdc by the end of the year, with over 900,000 individual projects delivering power each day. By the the time this report is published in Q1 2016, the U.S. will be approaching its millionth solar PV installation.

When accounting for all projects (both distributed and centralized), solar accounted for 29.4% of new electric generating capacity installed in the U.S. in 2015, exceeding the total for natural gas for the first time.

At the market segment level, 2015 was largely a continuation of ongoing trends.

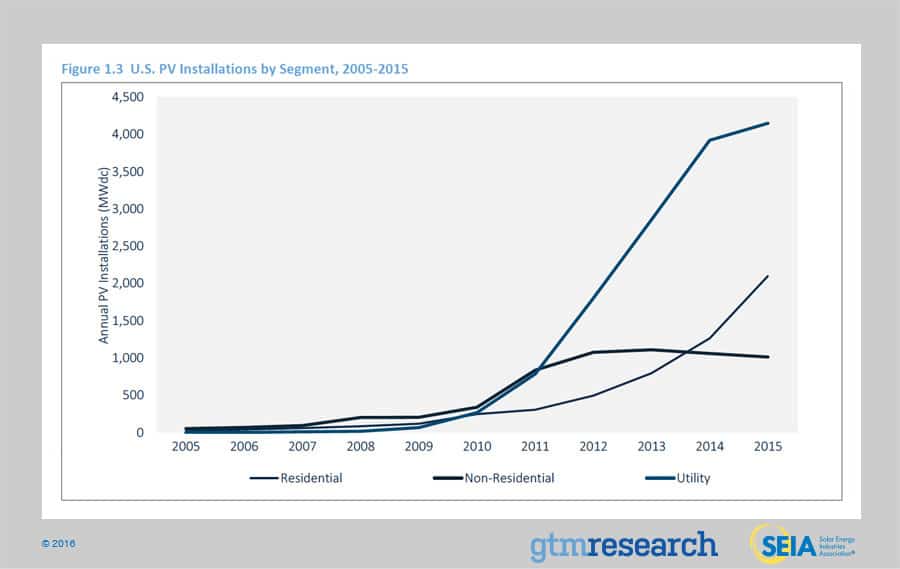

- Residential solar benefitted from a fourth consecutive year of >50% annual growth, with installations reaching 2,099 MWdc.

- Non-residential solar was essentially flat for the third year in a row, with 1,011 MWdc of installations. A mixture of market-specific factors and scaling challenges have plagued the sector, but numerous avenues remain for resumed growth over the coming year.

- Utility solar remained the largest segment by capacity, with 4,150 MWdc of installations in 2015. Even more notable than 2015 installation capacity is the current contracted project pipeline, which now exceeds 19.8 GWdc.

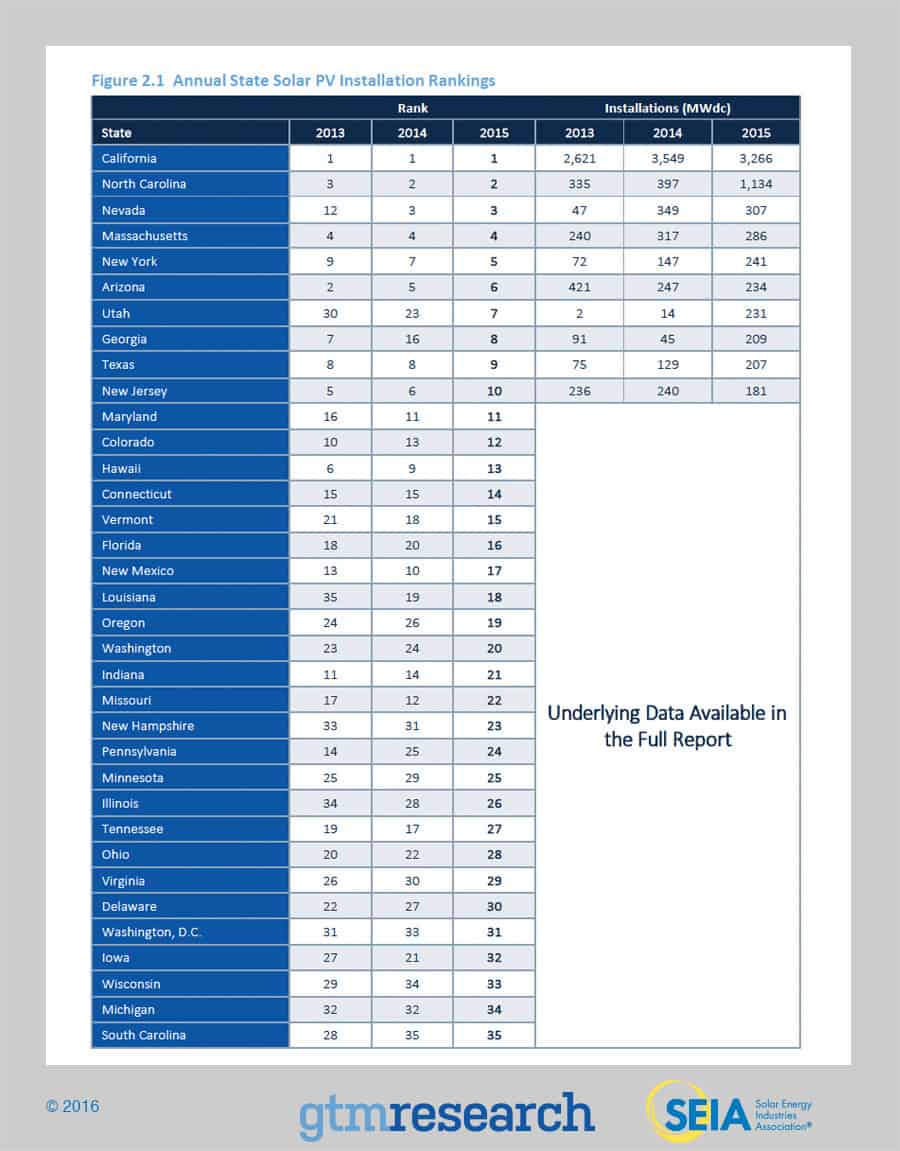

At the state level, the market remained relatively concentrated. The top 10 states accounted for 87% of all PV installations, and the top 20 states made up 96% of the market. But annual growth occurred in 24 of the 35 states we track individually, and 13 states installed over 100 MWdc of solar in 2015, up from nine in 2014. Six states (AZ, CA, MA, NV, NJ and NC) have surpassed 1 GW dc in cumulative solar capacity.

2015 was also a historic year for U.S. solar policy and regulation, with a number of decisions at both the state and federal level that will determine the trajectory of the market’s future growth.

First, the federal Investment Tax Credit was extended through 2021 in December, and a “commence construction” rule was added, effectively providing the market with policy visibility through 2023. GTM Research estimates that this extension alone will result in more than 50% net growth in U.S. solar installations from 2016-2020, an additional 24 GWdc over the five-year period. As a result of this change and other market developments since December, we now anticipate that cumulative solar photovoltaic installations will reach 97 GWdc by the end of 2020.

At the state level, net energy metering and electricity rate design came to the forefront of regulatory debates around solar in 2015, and a number of crucial decisions were reached. In California, the Public Utilities Commission (PUC) reached a final decision on the state’s next wave of net metering (dubbed NEM 2.0), which makes relatively modest modifications for solar customers including mandatory time-of-use rates and no more netting out of non-bypassable charges with solar. This ruling has largely been viewed as favorable for solar, while the opposite is true in Nevada, where the state PUC issued an order that increases customer fixed charges, lowers solar export compensation and, most controversially, applies to existing, in addition to prospective, solar customers. The Nevada decision remains in flux as this report is being published, with a number of legal challenges pending on both the NEM revisions and the lack of grandfathering.

Looking ahead to the rest of 2016, we anticipate another banner year for U.S. solar, which will benefit from gigawatts of utility PV that rushed through the early stages of development to ensure interconnection in 2016, in the event that the federal ITC stepped down to 10%. In turn, we forecast 16 GWdc of solar PV installations, up 120% over 2015, driven in large part by a utility PV market that will add more capacity than total solar installations brought on-line in 2015.

2. Photovoltaics

2.1. Market Segment Trends

2.1.1. Residential PV

2,099 MWdc installed in 2015, representing 66% growth over 2014

The residential PV market experienced its largest annual growth rate to date, an impressive feat given that 2015 marked the fourth consecutive year of greater than 50% annual growth.

Similar to prior years, California served as the primary driver of demand, fueling nearly 50% of annual residential PV installations. However, the residential market is showing glimpses of geographic demand diversification, with the number of 20 MWdc annual state markets for residential solar increasing threefold over the past four years.

But while a growing number of state markets are picking up steam, an even larger number of states are considering reforms to net metering rules that threaten the market’s ability to maintain a hockey-stick growth trajectory. Most recently, NEM reforms approved in Nevada are expected to drop the state from being the fifth-largest residential PV market in 2015 (based on annual installations) to the 31st in 2016.

2.1.2. Non-Residential PV

1,011 MWdc installed in 2015, down 5% from 2014

While residential solar’s impressive growth storyline continued in 2015, so did the non - residential PV market’s theme of flat demand. The continued stagnation in non-residential solar demand stems from states with either weak incentive funding or constrained development opportunities for 1+ MWdc projects. Amidst sluggish demand in most major state markets, the non-residential solar market became increasingly dependent on California, which experienced growth independent of state incentive funding thanks to solar-friendly rate structures and new development opportunities for 1+ MWdc projects.

Looking ahead, the 2016 rebound in non-residential PV demand will be supported by a triple-digit- megawatt pipeline of community solar projects, plus continued dependence on California to support nearly one-third of annual demand.

2.1.3. Utility PV

4,150 MWdc installed in 2015, representing 6% growth over 2014

The utility PV market continues to serve as the bedrock driver of installation growth in the U.S. solar market, accounting for 57% of capacity installed in 2015. Similar to prior years, demand was packed into the fourth quarter, with more utility PV capacity installed in Q4 2015 than the total U.S. solar installed in any prior quarter to date. This year, the Q4 boom was supported by developers in North Carolina rushing to complete projects ahead of an expiring in-state tax credit. In 2015, North Carolina became the first state besides California to add more than 1 GWdc of utility PV installations on an annual basis.

Looking ahead to 2016, the utility PV market is expected to nearly triple 2015 installations. Given a significant number of late stage projects with EPC agreements in place, in addition to the 5 GWdc already under construction, the utility PV market is expected to experience a sizable pull-in of demand despite the extension of the federal ITC.

With PPA prices for utility-scale solar already ranging between $35/MWh and $60/MWh, utility PV’s value proposition is evolving beyond simply meeting renewable portfolio standard (RPS) obligations. On top of RPS-driven demand, centralized PV is proving to be an economically competitive resource to meet utilities’ peak power needs. This is especially true in regions like Texas and the Southeast, where utilities are retiring their aging coal fleets and replacing them with utility PV, alongside combined-cycle natural gas plants.

2.2. National Solar PV System Pricing

We utilize a bottom-up modeling methodology to track and report national average PV system pricing for the major market segments. Though we continue to solicit weighted-average system pricing directly from utility and state incentive programs, we believe that this data less accurately reflects the current state of system pricing. Systems utilizing local incentive programs constitute a minority share of the market, and data from these sources often represents pricing quoted well prior to the installation and connection date.

Our bottom-up methodology is based on tracked wholesale pricing of major solar components and data collected from interviews with major installers, supplemented by data collected from utility and state programs.

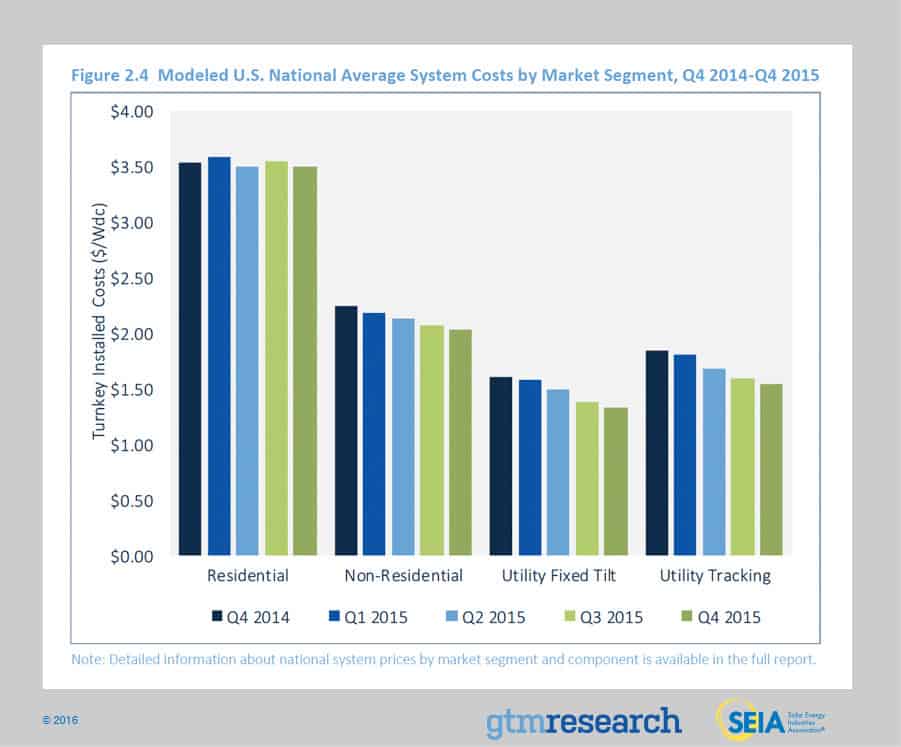

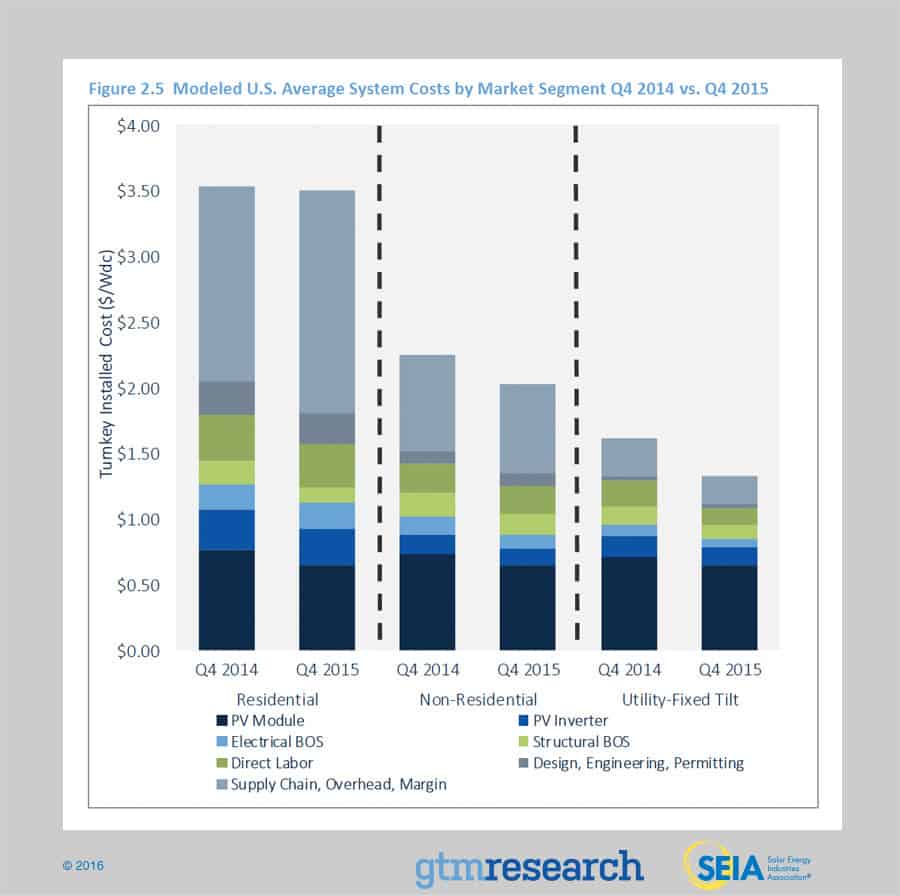

Overall system pricing fell by up to 17% over the course of 2015, depending on the market segment, with the largest declines in the utility fixed-tilt sector. On a quarterly basis, pricing continues to trend downward with some levelling-off in the residential sector in particular due to strong investment in customer acquisition and the stubbornness of other soft costs. In the non- residential and utility sectors, there were annual declines of 10% and 17%, respectively. This reflects continued aggressive cost reductions, both in hardware and soft costs, in national system pricing on an aggregate basis. Moreover, as installers and EPCs expand to regions with lower labor and regulatory compliance costs, these regions will have a larger impact on aggregate pricing. Due to advantages from scale, variations in utility system costs are much smaller than variations in residential and non-residential solar costs.

Average pricing for residential rooftop systems landed at $3.50/Wdc in Q4 2015, with nearly 65% of costs coming from on-site labor, engineering, permitting and other soft costs.

While residential hardware costs have fallen by over 16% in the past year, soft costs have actually risen on an industry average basis by 7%, primarily due to rising customer acquisition costs among national and local players alike.

In the non-residential market soft costs remain a challenge as well. Hardware costs fell 15% year- over-year while soft costs saw a modest decrease of 6%. In Q4 2015 soft costs accounted for approximately 50% of total system pricing. Soft costs can be even higher for projects in areas with strict labor requirements and particularly in tough permitting and interconnection jurisdictions. In order to continue reducing costs, developers and EPCs are looking to squeeze additional power density for commercial sites and amortize fixed costs over more power output – and therefore reduce dollar-per-watt and dollar-per-kWh.

Utility fixed-tilt and utility tracking projects in Q4 2015 saw an average cost of $1.33/Wdc and $1.54/Wdc, respectively. While utility system pricing is more tightly clustered than residential and non-residential system prices, state-by-state variation is prevalent. The Southeast U.S. led in terms of the lowest system costs, and the region played a significant role in bringing national pricing downward for utility fixed-tilt systems in 2015. Throughout the country, utility EPCs and developers continue to optimize their logistics and supply chains, as well as leveraging more mature installation practices, which has translated into major reductions in non-hardware costs across the board. In 2015, soft costs decreased 37% and 23% in fixed-tilt and tracking project, respectively.

2.3. Component Pricing

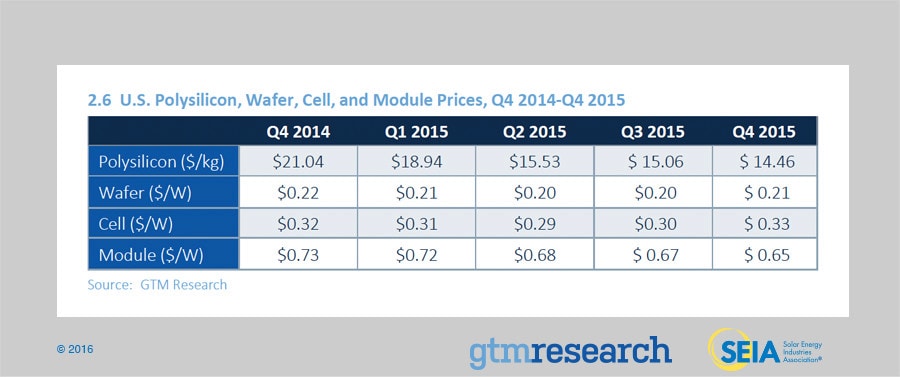

While a tight supply-demand market and stronger demand pull-in helped push wafer and cell prices up in Q4 2015, polysilicon and module prices continued to be impacted by aggressive price strategies.

- For polysilicon, prices fell 4% sequentially to $14.46/kg in Q4 2015. Inventory levels and aggressive end-of-year price strategies continued to affect global polysilicon prices. Average selling prices for U.S. producers were driven by the closure of the processing loophole in China, which reduced U.S. producers’ addressable market.

- Wafer prices were driven by strong demand pull-in and a tighter supply environment. This pushed wafer prices up 3% quarter-over-quarter to $0.21/W in Q4 2015.

U.S. module prices are largely driven by antidumping and countervailing duties on Chinese suppliers. In July 2015, the U.S. Department of Commerce filed its final review of the import tariffs on Chinese cells into the U.S. market. The final ruling set the cumulative duty at 30.61% for most major suppliers (21.70% for Yingli). During the fourth quarter, the average delivered price for Chinese modules ranged from $0.63/W on the low side (corresponding to order volumes greater than 10 MW for less established firms) to $0.65/W on the high side (established, bankable firms; order volumes of less than 1 MW). In 2016, prices are not expected to fluctuate as much as they did in 2015 due to expected strong demand pull-in. It should be noted that there is some price risk for producers that continue to ship all-Chinese products to the U.S. in 2016 as the tariff on Chinese cells may change again. Further, there is no assurance that the final results will resemble preliminary results (anti-dumping duties: 4.53% to 11.47%; countervailing duties: 19.62%).

2.4. Market Outlook

In December 2015, Congress passed an omnibus spending bill that included a multi-year extension of the federal Investment Tax Credit. Without question, the extension of the federal ITC ranks as the most important policy development for U.S. solar in almost a decade. Between 2016 and the end of the decade, the federal ITC extension will spur an additional 24 GWdc of PV capacity, positioning U.S. solar to become a 20 GWdc annual market by 2021.

Looking ahead, the federal ITC will remain at 30% through 2019, and then step down to 26% in 2020 and 22% in 2021. In 2022, it will step down to 10% for third-party-owned residential, non- residential, and utility PV projects, while expiring entirely for direct-owned residential PV. Equally important, projects that commence construction but do not interconnect in years 2019, 2020, and 2021 can qualify for correspondingly larger tax credits if they come on-line by the end of 2023.

Given the timing of the federal ITC extension, however, the wheels are already in motion for U.S. solar to benefit in 2016 from a double-digit-gigawatt pipeline of late-stage utility PV projects that rushed through development last year. In turn, we expect another record year for the U.S. PV market in 2016, with installations reaching 16 GWdc, a 119% increase over 2015. In 2017, while the residential and non-residential PV markets are both expected to grow year -over-year, the U.S. solar market is still expected to drop on annual basis due to the aforemention ed pull-in of utility PV demand in 2016.

In 2018, U.S. solar is expected to resume year-over-year growth across all market segments. And by 2021, more than half of all states in the U.S. will be 100+ MWdc annual solar markets, bringing cumulative U.S. solar installations above the 100 GWdc mark.

Forecast details by state (34 states plus Washington, D.C.) and market segment through 2021 are available in the full report.

3. Concentrating Solar Power

The final quarter of 2013 kicked off the first wave of mega-scale CSP projects to be completed over the next few years, and Q1 2014 built on that momentum, with 517 MWac brought on-line. This included BrightSource Energy’s 392 MWac Ivanpah project and the second and final 125 MWac phase of NextEra’s Genesis solar project. While Q2 2014 and Q3 2014 were dormant for CSP, Abengoa finished commissioning its 250 MWac Mojave Solar project in December 2014. As a result, 2014 ranked as the largest year ever for CSP, with 767 MWac brought on-line. In 2015, SolarReserve’s 110 MWac Crescent Dunes project, which entered the commissioning phase in February 2014, achieved commercial operation in November 2015.

With Crescent Dunes now on-line, near-term growth prospects for the CSP market in the U.S. are bleak. On one hand, CSP paired with storage represents an attractive generation resource for utilities, offering a number of ancillary and resource-adequacy benefits. However, due to extensive permitting hurdles that have confronted CSP project development timelines and federal ITC uncertainty in 2015, developers had put their CSP pipelines on hold.

Even with the federal ITC extension, the outlook for the CSP market will depend on further progress made toward mitigating early -stage development hurdles, lowering hardware costs, and strengthening the ancillary and capacity benefits provided by CSP paired with storage.

Acknowledgments

U.S. Solar Market Insight® is a quarterly publication of GTM Research and the Solar Energy Industries Association (SEIA)®. Each quarter, we collect granular data on the U.S. solar market from nearly 200 utilities, state agencies, installers and manufacturers. This data provides the backbone of this U.S. Solar Market Insight® report, in which we identify and analyze trends in U.S. solar demand, manufacturing and pricing by state and market segment. We also use this analysis to look forward and forecast demand over the next five years. All forecasts are from GTM Research; SEIA does not predict future pricing, bid terms, costs, deployment or supply.

- References, data, charts and analysis from this executive summary should be attributed to“GTM Research/SEIA U.S. Solar Market Insight®.”

- Media inquiries should be directed to Mike Munsell ([email protected]) at GTM Research and Alexandra Hobson ([email protected]) at SEIA.

- All figures are sourced from GTM Research. For more detail on methodology and sources, visit www.gtmresearch.com/solarinsight.

Our coverage in the U.S. Solar Market Insight reports includes 34 individual states and Washington, D.C. However, the national totals reported include all 50 states, Washington, D.C., and Puerto Rico.

Detailed data and forecasts for 34 states and Washington, D.C. are contained within the full version of this report, available at www.greentechmedia.com/research/ussmi.

AUTHORS

GTM Research | U.S. Research Team

Shayle Kann, Senior Vice President

MJ Shiao, Director of Solar Research

Cory Honeyman, Senior Solar Analyst (lead author)

Jade Jones, Senior Solar Analyst

Austin Perea, Solar Analyst

Colin Smith, Solar Analyst

Benjamin Gallagher, Solar Analyst

Scott Moskowitz, Solar Analyst

Solar Energy Industries Association | SEIA

Justin Baca, Vice President of Markets & Research

Shawn Rumery, Director of Research

Aaron Holm, Data Engineer

Katie O’Brien, Research Associate